As of the writing of this article, it appears likely that the lowered 1099-K threshold of $600 in gross payment amount will go into effect for tax year 2023. This is causing much anxiety among small sellers, and with good reason.

To help illustrate how much confusion and complexity is about to be created for small online sellers, we did research to identify some pretty common scenarios sellers might encounter that make for very interesting 1099-Ks and tax returns.

For example:

Inconsistent Gross Amount calculations

1099-Ks have been around since 2011. But did you know that, after 12 years, different platforms are still using different calculations in terms of what gets included in the Box 1 amount? See several examples as we look at the treatment of sales tax. Or check out our eBay 1099-K guide to see how even eBay provides different numbers in different places.

Selling personal items among your business inventory

Do you track your personal sales separately from your business sales? Because eBay, Poshmark and others don’t. You get a single 1099-K for all sales on each platform. Yet what if you sold some personal items at a loss? Personal items don’t get treated the same as normal business sales. We took a deep dive into this scenario, to help walk sellers through what to do.

Consignment sales

As a reseller of someone else’s items, you may be collecting the full amount of the sale, which will be reported on your 1099-K. Except your income is really only the commission you receive from the sale. How are you supposed to account for this? Learn more as we share what we’ve uncovered.

Don’t stress

Our intent in pulling these example together is not to increase fear or anxiety. We believe there is ample evidence that the entire situation is imperfect, and what the IRS cares the most about is that you pay the correct amount of tax that your business owes. With reasonable bookkeeping, it shouldn’t be too hard to handle these scenarios. At Seller Ledger, we pull in your detailed sales and expense information to make this as simple as possible. We also offer a 30-day free trial, no credit card required.

It is our belief that Congress does not fully understand the unnecessary complexity they have created, especially for small sellers. So, we encourage sellers to get involved and send a message to Congress. Click either of the buttons below to be taken to a place to make your voice heard:

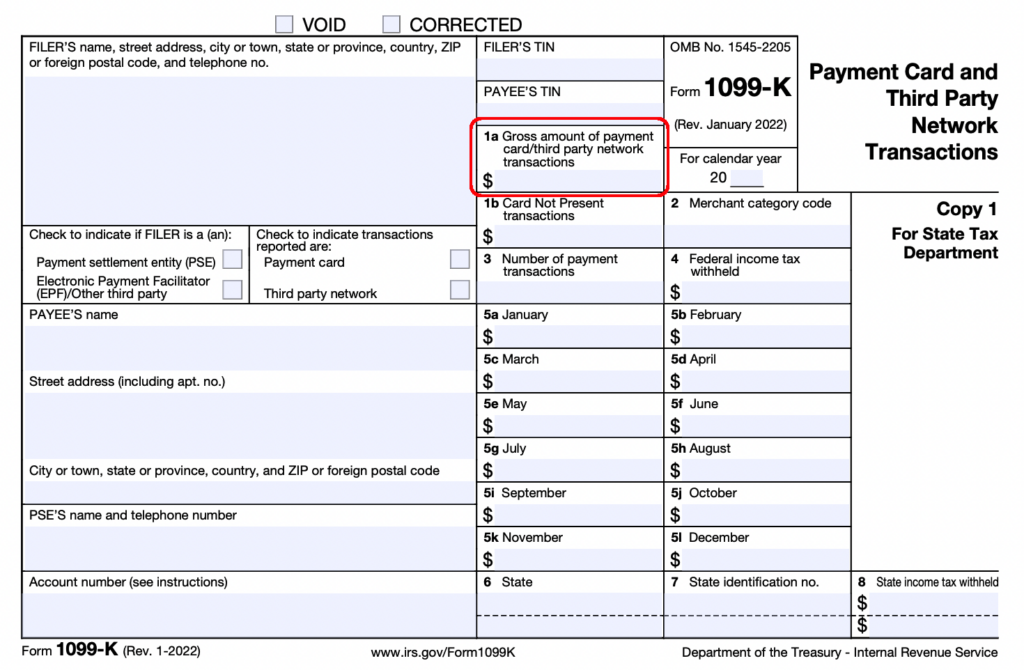

Back when we first launched, we wrote a blog post about 1099-Ks and where sellers can expect to find the amounts that make up the total in Box 1a (Gross amount of payment card/third-party network transactions.) At the time, we were referencing eBay’s calculations.

But, as we approach the end of the tax year, we’ve learned that different platforms calculate their Box 1a amounts differently, often around whether or not sales tax collected is included.

Below is a sample of our findings – if you discover more and want to pass them along, we’re happy to update the list.

Sales tax NOT included in Box 1a

For example, the following platforms indicate in their documentation that sales tax is likely NOT included in the gross amount reported to the IRS:

Ebay

In their help page, eBay states: “Additionally, Form 1099-K does not include the sales tax when it is automatically collected and remitted by eBay.”

Poshmark

This support page from Poshmark states: “Your Form 1099-K will only include income as calculated by gross sales (including fees, refunds, and cancelled orders) on the Poshmark platform.”

Etsy

Their help page is a bit less clear, stating that the gross sales includes “Sales tax collected by you.” However, just below that, they make this statement: “In some cases, Etsy collects sales tax from buyers and remits it to tax authorities on behalf of sellers. If Etsy has collected tax on your behalf, these amounts won’t appear on your 1099-K form.”

Sales tax included in Box1a

However, other platforms either don’t spell it out very clearly or imply the opposite – that sales tax collected IS included in the Box 1a amount:

This page from their help center states that their Unadjusted Gross Payment combines various amounts, including: “Sales tax charged to buyer (a separately stated sales tax paid by the Buyer at the time of purchase and remitted directly to the state under Mercari’s sales tax registration)”

Square, Shopify and likely most shopping cart platforms

The IRS’s own instructions for Schedule C provides a great starting point for confusion. Looking at the instructions for Line 23 (expenses for taxes and licenses,) you will find the following two statements:

You can deduct the following taxes and licenses on this line.

State and local sales taxes imposed on you as the seller of goods or services. If you collected this tax from the buyer, you must also include the amount collected in gross receipts or sales on line 1.

and

Do not deduct the following.

State and local sales taxes imposed on the buyer that you were required to collect and pay over to state or local governments. These taxes are not included in gross receipts or sales nor are they a deductible expense. However, if the state or local government allowed you to retain any part of the sales tax you collected, you must include that amount as income on line 6.

Clear as mud, right?

Adding to the confusion, there are statements from some “experts” that it’s critical to have your tax return line up with the forms that the IRS receives. But if you are a multi-channel seller, and the IRS receives multiple 1099-Ks that are based on different calculations, how are you supposed to get your amounts to line up?

It is unlikely that members of Congress understood the full potential for inconsistency when they introduced Form 1099-K for the 2011 tax year. Yet it has remained relatively unchanged for the last 12 years. And now, with the threshold for “gross amount” dropping to $600, this confusion will impact more small sellers than ever.

It doesn’t have to be a big deal

From our perspective, what’s most important is that you get to the correct amount of tax owed. That’s where good bookkeeping comes into play. If you are a multi-channel seller facing the possibility of receiving multiple 1099-Ks that included different numbers (like sales tax,) it becomes critical to have the order-level details (product price, any discounts, shipping, sales tax collected, fees charged, etc) broken out and properly categorized so that you can sub-total by any or all of them. This way, should anyone come asking, you can produce accurate reports of every total, and even drill down to the specific transactions behind them.

With Seller Ledger, we automatically import order-level details from the top online sales channels, along with banks and credit cards, to help you produce a Schedule C tax report that is accurate for your business. Anyone can try Seller Ledger free for 30-days, no credit card required.

As part of our efforts to further research interesting 1099-K scenarios, we wanted to explore a question that many resellers have recently asked about: consignment sales.

What are consignment sales?

A consignment sale happens when a reseller (called the consignee) helps another individual or business (called the consignor) sell some of their products for them. Usually, the owner of the products (consignor) compensates the reseller (consignee) by paying a percentage of the total sale, a flat fee, or some other negotiated rate.

Conceptually, this arrangement is pretty straightforward. The issue is: how does the accounting work? And where do 1099-Ks come into play?

Accounting for consignment sales – before 1099-Ks

Traditionally, the way to handle accounting of consignment sales is as follows:

The owner of the item (consignor) tracks the total sale as income, and treats the commission paid to the person selling it on their behalf (consignee) as an expense. The consignee just reports the commission amount as their income. In fact, if the consignor sends the consignee more than $600 in commission payments, there’s a good chance of them sending the consignee a 1099.

Why does the accounting normally work like this? Because ownership of the item (officially referred to as “title”) does not pass from the business to the reseller when consigned. The original owner still has “title” to the item until it sells, at which point it transfers to the buyer. So the sale gets recorded as a sale from the owner (consignor) to the end buyer, and the commission gets paid to the reseller (consignor.)

Let’s look at an example:

A local small business has an armoire, originally purchased for $100, that they would like to sell on consignment. They enlist a reseller, who agrees to sell the item in exchange for a 20% commission. That reseller successfully sells the armoire for $300. Ignoring things like shipping costs and fees, the resulting accounting entries would look this:

Owner/Consignor:

Product sales: $300

- Cost of Goods Sold: $100

- Commission: $60 (paid to Reseller/Consignee)

===========================

= Net profit: $140

Reseller/Consignee:

Commission income: $60 (received from Owner/Consignor)

===========================

Net profit: $60

This, however, raises an interesting question: if the consignee is collecting the money for the sale, how do they only report $60 of income?

Now you start to see why this is confusing in the world of eCommerce and 1099-Ks. We won’t get too far into the details (unless enough people ask,) but the key concept is that, as a consignee, when you collect the money from a consignment sale, that money doesn’t get counted as your revenue. It’s actually a liability. You owe it to the consignor (less any commission and agreed-upon costs) as soon as you collect it. Only the commission is income.

And herein lies the point of the article. If you are an eCommerce reseller doing consignment sales, the platform you are selling on knows nothing about consignment. They will send you a 1099-K that includes the total sales proceeds. In the above case, that would be the full $300.

So what should you do?

Accounting for consignment sales – matching 1099-Ks

Disclaimer

Before proceeding it’s important to mention that we at Seller Ledger are not tax experts and are not trying to provide tax advice. It is critical that you as a reader make your own decisions on how to handle your specific tax situation, which may include hiring a professional.

First, the fact that 1099-Ks from a platform like eBay do not exactly match your sales records is okay. The 1099-K is an informational form. The IRS knows that it may not represent a business’s true income. Therefore, accurate bookkeeping is critical.

When the sale shows up from your online sales channel, you can go ahead and categorize it as product sales, and when you make your payment to the original owner/consignor for the net amount minus your commission, make sure to categorize that properly.

“Do not include merchandise you receive on consignment in your inventory. Include your profit or commission on merchandise consigned to you in your income when you sell the merchandise or when you receive your profit or commission, depending upon the method of accounting you use.”

Mark Tew, of NotYourDadsCPA, suggests using “Commissions” in this video, which we think makes a lot of sense.

Using the same scenario as above, this would result in entries that look like this:

Reseller/Consignee:

Product sales: $300

- Commissions: $240 (paid to the Owner/Consignor)

===========================

= Net profit: $60

Owner/Consignor:

Product sales: $240 (received from Reseller/Consignee)

- Cost of Goods Sold: $100

===========================

= Net profit: $140

Note that each party’s net profit is still the same – the accounting entries are just a bit different. As a reseller, what matters most is that your bottom line profit accurately reflects the business that you did. And taking this approach will help your top-line numbers match the 1099-Ks that get reported for your business.

Simplify your bookkeeping

At Seller Ledger, we import the individual order details of everything you sell through your online sales channels, making it easy to spot those consignment sales and categorize the payouts to consignors properly. Once you have categorized an expense with a consignor, Seller Ledger’s software can remember this for you so all future sales expenses with that consignor can be treated the same way. Anyone is welcome to try Seller Ledger for 30 days, free of charge with no credit card required.

To help track consignment agreements and payouts, we have launched a new, free extension to the Seller Ledger application at consign.sellerledger.com. Seller Ledger customers who sell on consignment can now track how much they owe in consignment commissions by identifying which eCommerce sales belong to which consignor. Help us perfect this important customer need – check it out now.

By now, most small eCommerce sellers are aware that the annual sales threshold for receiving a 1099-K from online payment platforms is dropping to $600. There is a lot of content out there about what is included in the 1099-K amount, how that can vary from one platform to the next, and ways to make sure you’re capturing the right deductions.

But a very interesting question that we’ve heard from customers is: how do you handle sales of personal items?

When most new sellers are getting started, they begin by listing some (or many) personal items. It’s a great way to learn the ropes. Over time, they start making their own products for sale or sourcing items for resale from other places. But there’s still a good chance that, even among sellers who have been doing this for years, some personal items are bound to get listed.

Personal vs Business items

The most important difference between selling personal items versus those you’ve purchased for the purposes of resale is this: you cannot claim a loss on the sale of personal items.

The IRS is happy to tax the profit on both personal and business items, but you can only declare a loss on items you specifically built or purchased with the intent to resell (e.g. your inventory.) Items used for personal reasons, even if they are sold for less than the amount you originally paid, do not create a loss.

Let’s talk about a few examples:

Personal item sold for a profit

You have a copy of a now out-of-print vinyl album that you bought WAY back in the day for maybe $10. After listening to it a few times, you socked it away and didn’t think much about it. However, you one day discover it’s a bit of a collectors item, so sell it online for $17.50. In this case, you would owe tax on the $7.50 in profit.

Revenue: $17.50

Cost of goods sold: $10.00

Profit: $7.50

Business item sold for a profit

Let’s take that same scenario, but instead say you found an out-of-print vinyl record at a yard sale for $10. You also sold it for $17.50. The scenario would be identical:

Revenue: $17.50

Cost of goods sold: $10.00

Profit: $7.50

Business item sold for a loss

Now let’s say, in your sourcing, you find another out-of-print vinyl album that costs $10 and are sure you can sell it for a profit. But when the time comes, you can’t get more than $5 for it. So, you take your $5 and call it a day. Here, the scenario would differ:

Revenue: $5.00

Cost of goods sold: $10.00

Loss: $5.00

Because you purchased that album with the intent to resell it, and didn’t use it for personal enjoyment, you can write off that loss against other profitable sales.

Personal item sold for a loss

Going back to that original example, let’s say that that old vinyl record you only listened to a few times turned out to be worth only $5. You take the money and free up some space in the house. Now, you might think that accounting for it might be the same as the preceding example – but that would be incorrect.

Revenue: $5.00

Cost of goods sold: $10.00?

Loss: NOT ALLOWED

The IRS states very clearly, in it’s Understanding your 1099-K guidance: “A loss on the sale of a personal item isn’t deductible.”

Ok, so what should you do?

Disclaimer

Before proceeding it’s important to mention that we at Seller Ledger are not tax experts and are not trying to provide tax advice. It is critical that you as a reader make your own decisions on how to handle your specific tax situation, which may include hiring a professional.

Calculating the cost of personal items sold at a loss

They also describe how you could file these amounts as a $0.00 capital gain on Form 8949.

Notice that neither option mentions Schedule C. This is a big part of why this all gets so confusing. These examples provided by the IRS assume that your 1099-K came ONLY from the sale of personal items. But, more commonly for online sellers, the sale of personal items is just a small part of their broader business inventory sales. So how should you file?

Form options and their bookkeeping requirements

Option 1: Track the personal item sales separately and include them on Schedule 1 (or Form 8949) of your 1040.

If you want to follow the IRS instructions precisely, you can track the sale of your personal items separately. However, this will require additional record keeping effort, and could result in amounts that don’t match the 1099-K totals received.

Option 2: Include the sale of personal items in your Schedule C

This option likely keeps the 1099-K totals consistent, and requires less record keeping complexity, but you will need to make sure to identify those personal item sales and make sure the cost is “up to but not more than the proceeds amount“

There may be other options available to you, so it’s important to talk with a tax professional about your desired choice.

How Seller Ledger can make this easier

Now, not to persuade you one way or another, but Seller Ledger actually makes Option 2 above pretty easy.

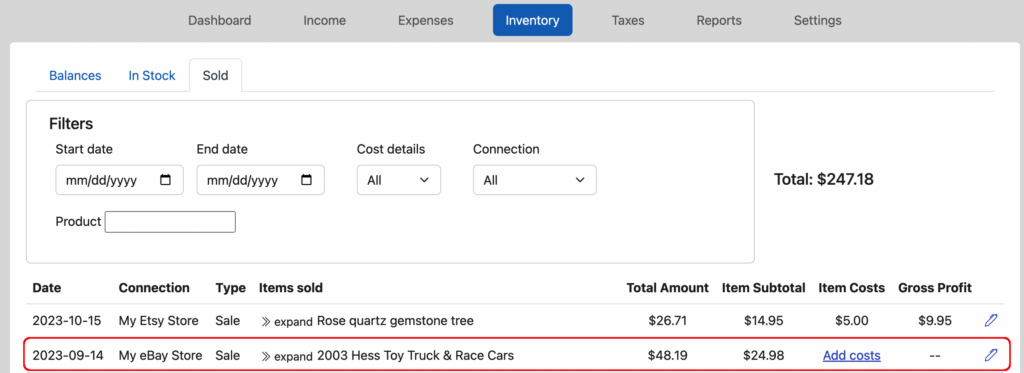

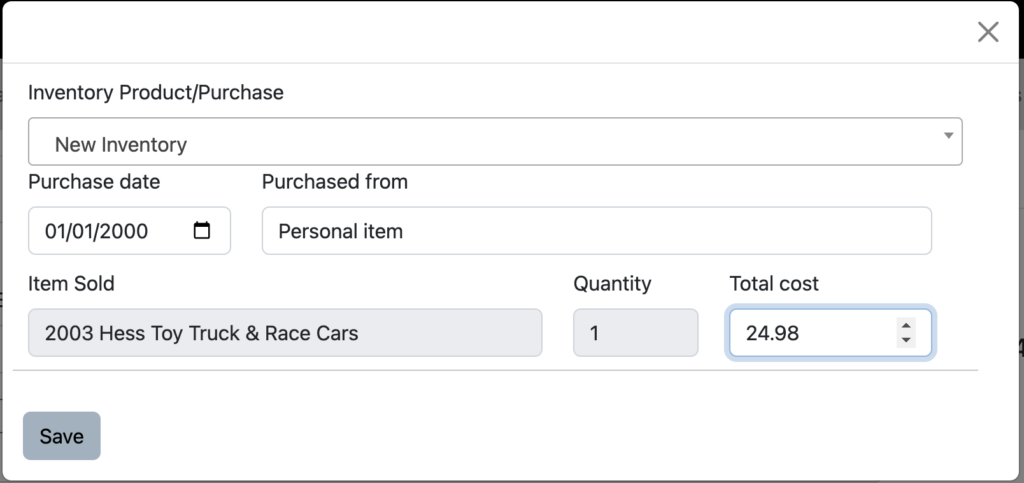

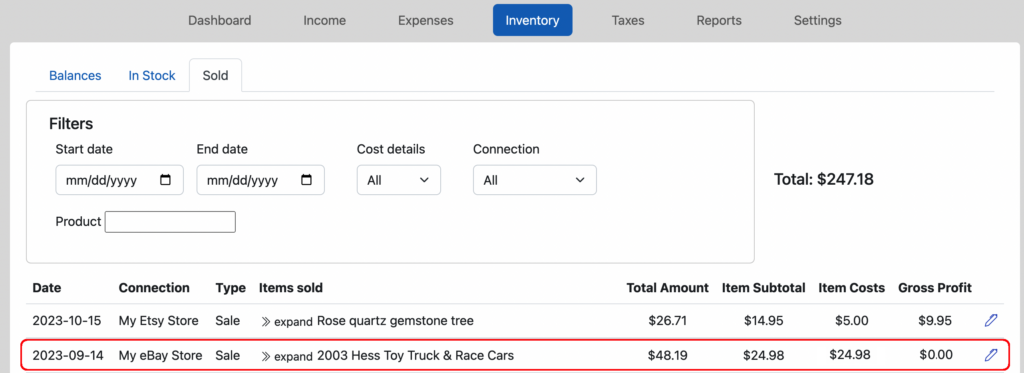

As part of our rollout of support for inventory and cost of goods tracking earlier this year, we introduced a view of your Sold items that allows you to enter the cost information even after an item has sold. While this provides the opportunity to match that sale to prior inventory purchases, it also allows you to enter items that were never in your business inventory. For example, personal items that you sold. And since we show you the item subtotal right there (what that item sold for,) you can just add your personal item and enter the subtotal amount as the cost. When you click save, your “Gross profit” on that item will show $0.00 – just like in the IRS guidance.

Click “Add costs” from the Sold view:

Enter the cost for that item that matches the Item Subtotal

See your Gross Profit show $0.00.

If you want help automating your eCommerce bookkeeping, we do offer a free 30-day trial, no credit card required. We automatically import your sales and expense history from Amazon, eBay, Etsy and Poshmark, as well as bank and credit card transactions.

We are proud to announce that Seller Ledger now connects directly with your Amazon Seller Central account to help automate much of your Amazon business accounting. As with eBay and Etsy, you can link your Amazon Seller Central account to Seller Ledger and we’ll regularly import your sales and expenses and automatically categorize them for you. Just log into your dashboard and click the “Add Account” button to link your Amazon account.

Also, like with eBay and Etsy, you can always change how you’d like to see your Amazon information categorized by customizing your settings.

Thanks again to the customers who helped us in testing this new integration. Amazon did limit the number of people we could link during the beta period, so we may yet see some new transaction types. If this happens, you may see your Amazon import pause, and we’ll be notified on the back-end to add support for the new transaction type.

Amazon has also listed us in their Selling Partner Appstore, where customers are able to learn more about the product and leave reviews. We’re big fans of customer word of mouth, so if you have an opinion about Seller Ledger and would be willing to share it with other prospective customers, please do.

Next up:

We’re actively working on a Mercari import solution (similar to what we recently announced with Poshmark) and the ability to upload CSV files for poorly or unsupported banks. If you would be interested in beta testing either of these features, please email us at [email protected].

Small online sellers who generate more than $600 a year in receipts get to breathe a sigh of relief…for one more year.

On December 22, 2022, the IRS delayed the implementation of the $600 threshold for payment platforms to provide 1099-Ks for online sellers. Instead of receiving 1099-Ks in early 2023 for the 2022 tax year, everything is being pushed back a full year.

For the 2022 tax year, the same thresholds of $20,000 in payments received from more than 200 transactions apply.

Last year, the IRS made a major change that will send a LOT more 1099-Ks to small online sellers.

Prior to this change, only sellers who had at least $20,000 in gross receipts across more than 200 transactions in a year would received a 1099-K. Some states have already lowered the threshold.

As part of the American Rescue Plan of 2021, this threshold was changed to a mere $600 per year. That means nearly all online sellers should expect to receive a 1099-K going forward. The change was originally intended to take effect for the 2022 tax year, but small sellers just got a slight reprieve as the IRS pushed back implementation by a year.

What’s the big deal?

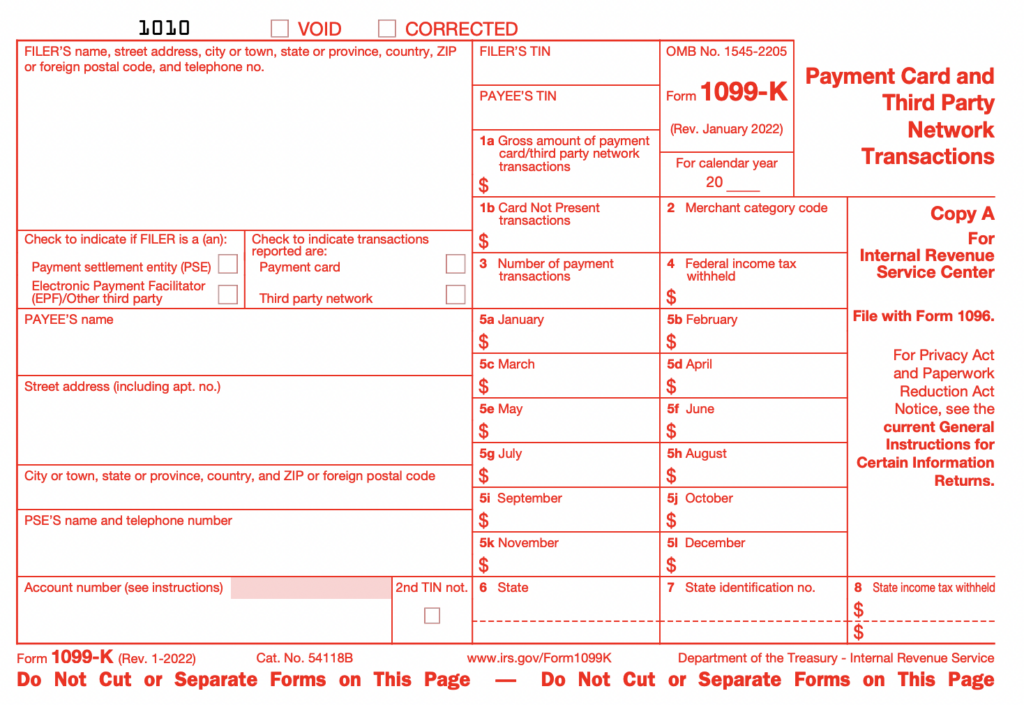

Should small online sellers dread the 1099-K?

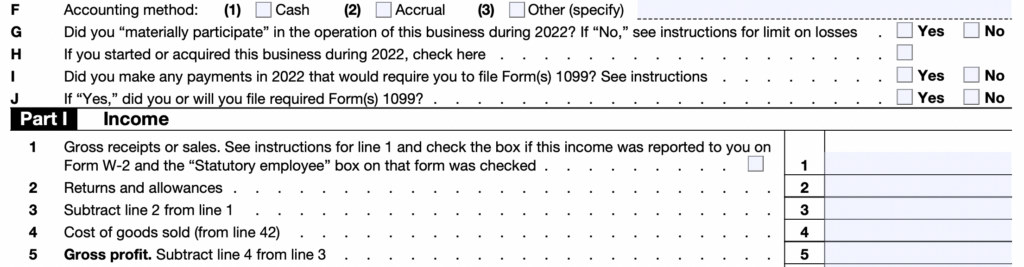

The primary concern for many sellers is that a 1099-K means they will owe taxes on the amount reported in Box 1a (see the image above.) Sellers are also concerned about reporting the correct amount on Line 1 of their Schedule C (see image below) and matching that amount to their 1099-K.

It’s better when numbers match

Avoiding mismatched numbers

Here are some things that could cause differences and what you can do to avoid them:

Shipping

Box 1a of the 1099-K WILL include shipping amounts that you collect from the buyer. You should make sure that these amounts are also included in Line 1 of your Schedule C. Additionally, you’ll want to be sure you’re tracking and reporting all of your actual shipping costs as expenses.

Transaction Fees

Box 1a of the 1099-K WILL NOT include any fees that may have been taken out of your order (e.g. final value fees, transaction fees, etc.) This means the amount you actually receive in your bank account will be less than what gets reported to the IRS. Therefore, it’s very important to keep track of all of your selling fees and report them as expenses.

Refunds and Discounts

Like with fees, Box 1a WILL NOT include refunds and discounts. It is up to you to keep track of these separately, and place the total amount in Line 2 of your Schedule C tax form.

Multiple channels and multiple payment providers

It’s important to remember that each payment platform will be sending 1099-Ks to any sellers with more than $600 in annual transactions. If you sell on multiple channels, and they use different payment processors, you are likely to receive multiple 1099-Ks. In an ideal world, the sum of the 1099-K amounts should equal Line 1 on your Schedule C. However, this assumes that each payment platform treats all of these numbers the same. If anyone finds examples where this isn’t true, please shoot us an email and we’d be happy to dig into it and see what’s going on, then share with the broader community.

What about Sales Tax?

There seem to be many questions about whether sales tax should be included in Box 1a. Based on 1099-Ks shared with us by customers, and language from eBay’s help website, sales tax that is both collected and remitted for you will not be included.

Good bookkeeping makes this much easier to handle

While you can’t control what gets reported to the IRS, you can control what you file on your tax return. You can ensure the numbers in your tax return match what the IRS sees through good bookkeeping practices. If you are looking for help on that front, consider Seller Ledger, a bookkeeping program that’s specifically designed for online sellers. Seller Ledger’s automated solution breaks out those shipping, refund and fee details and make sure they roll up to the correct tax lines to match the 1099-K.

Disclaimer

The content in this page should not be construed as legal or tax advice. Please consult an attorney or tax professional regarding your specific tax situation.