Accounting for Personal Item Sales That are Included in Your 1099-K

By now, most small eCommerce sellers are aware that the annual sales threshold for receiving a 1099-K from online payment platforms is dropping to $600. There is a lot of content out there about what is included in the 1099-K amount, how that can vary from one platform to the next, and ways to make sure you’re capturing the right deductions.

But a very interesting question that we’ve heard from customers is: how do you handle sales of personal items?

When most new sellers are getting started, they begin by listing some (or many) personal items. It’s a great way to learn the ropes. Over time, they start making their own products for sale or sourcing items for resale from other places. But there’s still a good chance that, even among sellers who have been doing this for years, some personal items are bound to get listed.

Personal vs Business items

The most important difference between selling personal items versus those you’ve purchased for the purposes of resale is this: you cannot claim a loss on the sale of personal items.

The IRS is happy to tax the profit on both personal and business items, but you can only declare a loss on items you specifically built or purchased with the intent to resell (e.g. your inventory.) Items used for personal reasons, even if they are sold for less than the amount you originally paid, do not create a loss.

Let’s talk about a few examples:

Personal item sold for a profit

You have a copy of a now out-of-print vinyl album that you bought WAY back in the day for maybe $10. After listening to it a few times, you socked it away and didn’t think much about it. However, you one day discover it’s a bit of a collector’s item, so you sell it online for $17.50. In this case, you would owe tax on the $7.50 in profit.

Revenue: $17.50

Cost of goods sold: $10.00

Profit: $7.50Business item sold for a profit

Let’s take that same scenario, but instead say you found an out-of-print vinyl record at a yard sale for $10. You also sold it for $17.50. The scenario would be identical:

Revenue: $17.50

Cost of goods sold: $10.00

Profit: $7.50Business item sold for a loss

Now let’s say, in your sourcing, you find another out-of-print vinyl album that costs $10 and are sure you can sell it for a profit. But when the time comes, you can’t get more than $5 for it. So, you take your $5 and call it a day. Here, the scenario would differ:

Revenue: $5.00

Cost of goods sold: $10.00

Loss: $5.00Because you purchased that album with the intent to resell it, and didn’t use it for personal enjoyment, you can write off that loss against other profitable sales.

Personal item sold for a loss

Going back to that original example, let’s say that that old vinyl record you only listened to a few times turned out to be worth only $5. You take the money and free up some space in the house. Now, you might think that accounting for it might be the same as the preceding example – but that would be incorrect.

Revenue: $5.00

Cost of goods sold: $10.00?

Loss: NOT ALLOWEDThe IRS states very clearly, in its Understanding your 1099-K guidance: “A loss on the sale of a personal item isn’t deductible.”

Ok, so what should you do?

Disclaimer

Before proceeding it’s important to mention that we at Seller Ledger are not tax experts and are not trying to provide tax advice. It is critical that you as a reader make your own decisions on how to handle your specific tax situation, which may include hiring a professional.

Calculating the cost of personal items sold at a loss

The IRS, in their 1099-K Frequently Asked Questions, also states:

“Report your costs, up to but not more than the proceeds amount“

This would imply the following way of recording that sale:

Revenue: $5.00

Cost of goods sold: $5.00 (no more than the proceeds amount)

Profit/Loss: $0.00In fact, the IRS provides specific examples and how to file them. From their 1099-K guidance:

Schedule 1 (form 1040)

Enter the Form 1099-K gross payment amount (Box 1a) on Part I – Line 8z – Other Income: “Form 1099-K Personal Item Sold at a Loss, $700”

Offset the Form 1099-K gross payment amount (Box 1a) on Part II – Line 24z – Other Adjustments: “Form 1099-K Personal Item Sold at a Loss $700”

You can view the full Schedule 1 here.

They also describe how you could file these amounts as a $0.00 capital gain on Form 8949.

Notice that neither option mentions Schedule C. This is a big part of why this all gets so confusing. These examples provided by the IRS assume that your 1099-K came ONLY from the sale of personal items. But, more commonly for online sellers, the sale of personal items is just a small part of their broader business inventory sales. So how should you file?

Form options and their bookkeeping requirements

Option 1: Track the personal item sales separately and include them on Schedule 1 (or Form 8949) of your 1040.

If you want to follow the IRS instructions precisely, you can track the sale of your personal items separately. However, this will require additional record keeping effort, and could result in amounts that don’t match the 1099-K totals received.

Option 2: Include the sale of personal items in your Schedule C

This option likely keeps the 1099-K totals consistent, and requires less record keeping complexity, but you will need to make sure to identify those personal item sales and make sure the cost is “up to but not more than the proceeds amount“

There may be other options available to you, so it’s important to talk with a tax professional about your desired choice.

How Seller Ledger can make this easier

Now, not to persuade you one way or another, but Seller Ledger actually makes Option 2 above pretty easy.

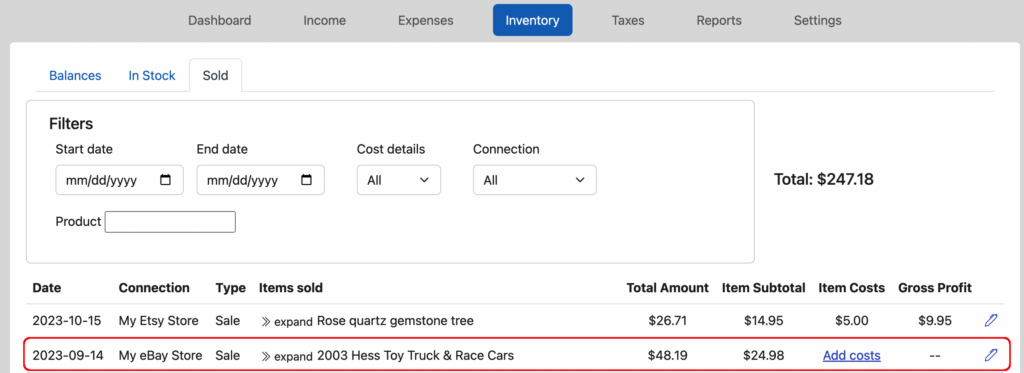

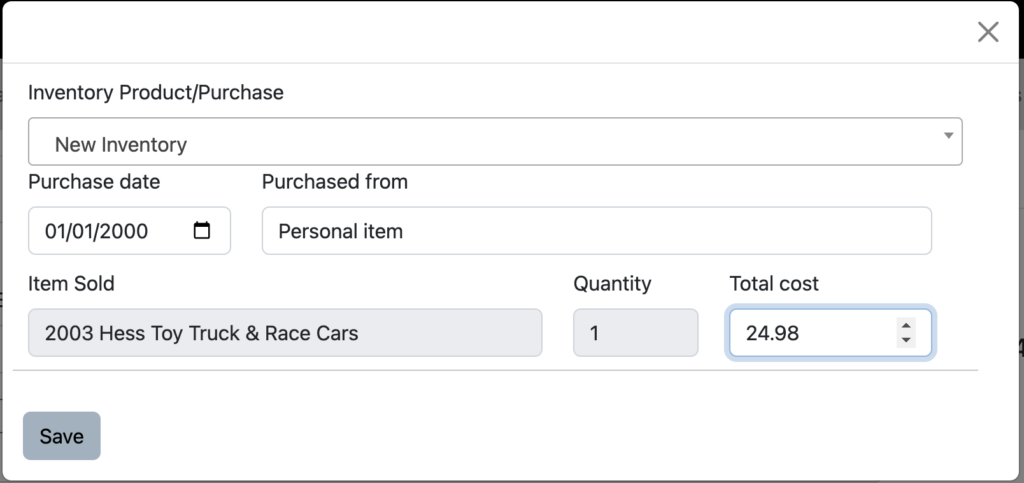

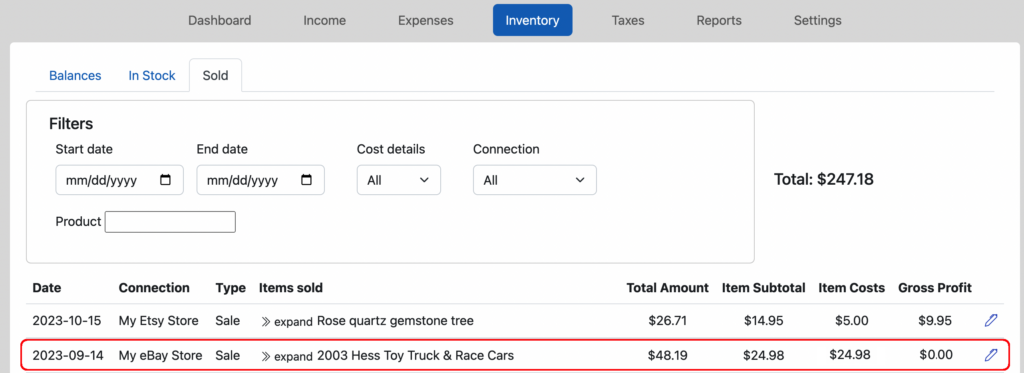

As part of our rollout of support for inventory and cost of goods tracking earlier this year, we introduced a view of your Sold items that allows you to enter the cost information even after an item has sold. While this provides the opportunity to match that sale to prior inventory purchases, it also allows you to enter items that were never in your business inventory. For example, personal items that you sold. And since we show you the item subtotal right there (what that item sold for,) you can just add your personal item and enter the subtotal amount as the cost. When you click save, your “Gross profit” on that item will show $0.00 – just like in the IRS guidance.

Click “Add costs” from the Sold view:

Enter the cost for that item that matches the Item Subtotal

See your Gross Profit show $0.00.

Stay tuned for more posts as we head into tax season. We’ll do our best to provide more research into ways to make tax season less stressful.

Ready to automate your eCommerce bookkeeping?

Join thousands of sellers who save hours every month with Seller Ledger.

No credit card required