Consignment Accounting

A while back, we wrote a pretty in-depth blog post about consignment sales and 1099ks. Since then, we’ve had a number of questions from customers about how to properly track consignment sales in Seller Ledger. And we’ve added a LOT of functionality to make that easier, so let’s dive right in.

It’s not inventory

The first thing to realize when dealing with consignment sales, is that, even if you are temporarily taking possession of the items to sell, they do not count as inventory because they never belong to you. While this may seem odd, it’s actually pretty freeing from a tracking perspective.

Instead, all you need to do is keep track of the consignment items that sell, and the net profit from each of those sales, and how much you owe to the consignor.

Fortunately, Seller Ledger automates most of that.

Net profit of each sale

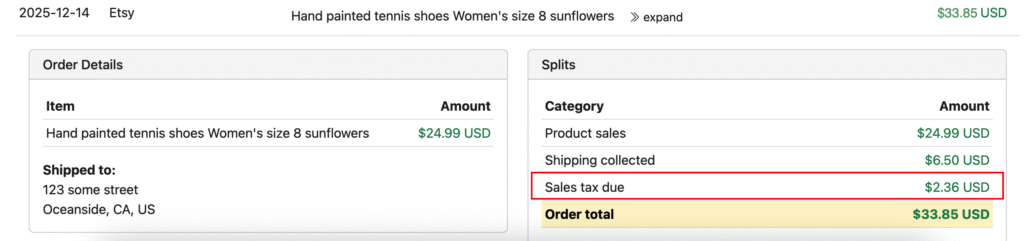

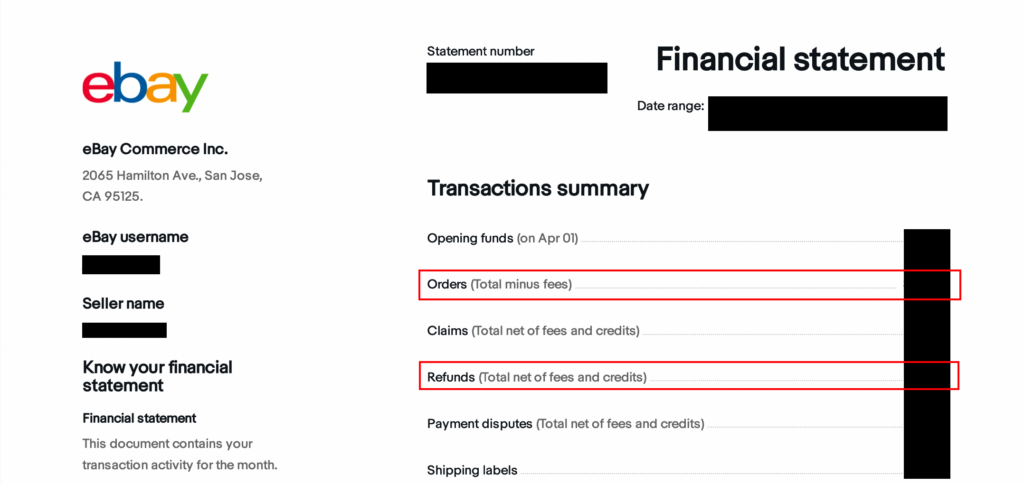

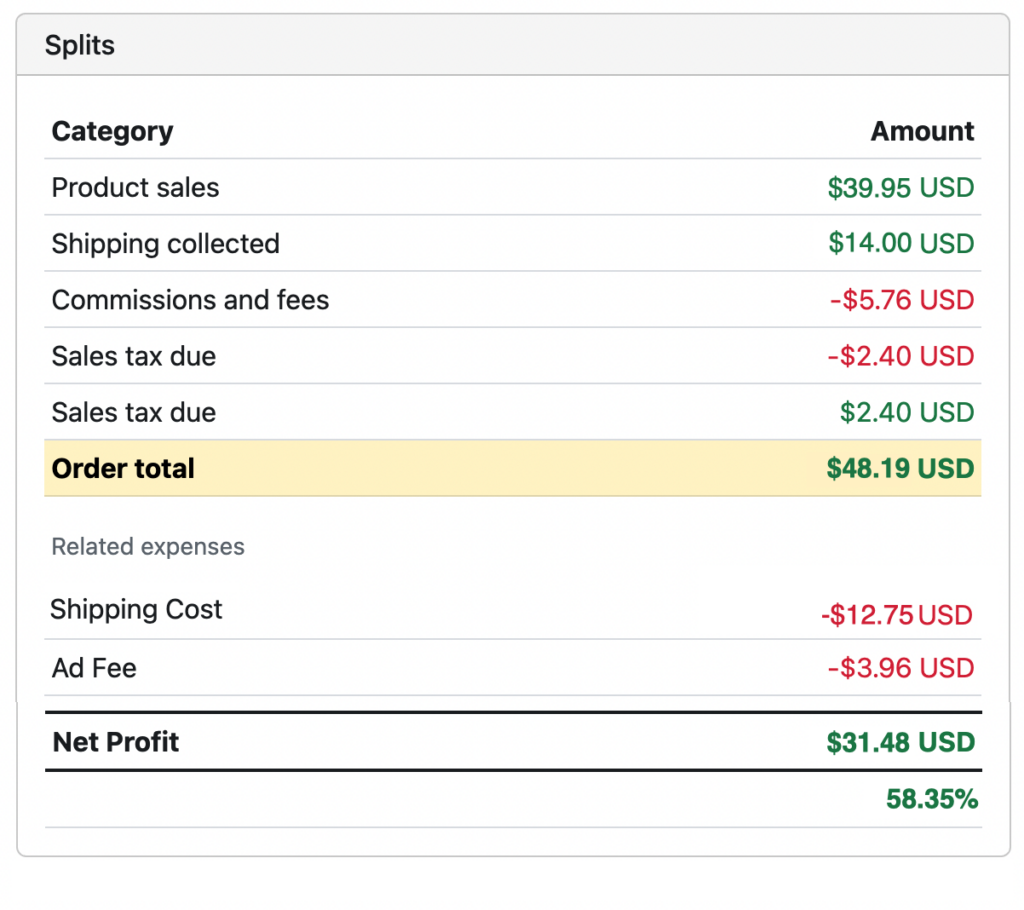

Most consignees (the people doing the selling on behalf of someone else,) negotiate payment terms based on the money earned AFTER subtracting costs like shipping and fees. Normally, this requires a lot of time spent in spreadsheets. But for many online sales channels, Seller Ledger does this for you automatically. We import the sale price, any shipping label costs, order-related fees – everything. See how we do it for eBay, Amazon, Walmart and other platforms.

In this case, let’s say you were doing a 50/50 split with the consignor. That would mean sending her/him $15.74.

Categorizing consignor payments

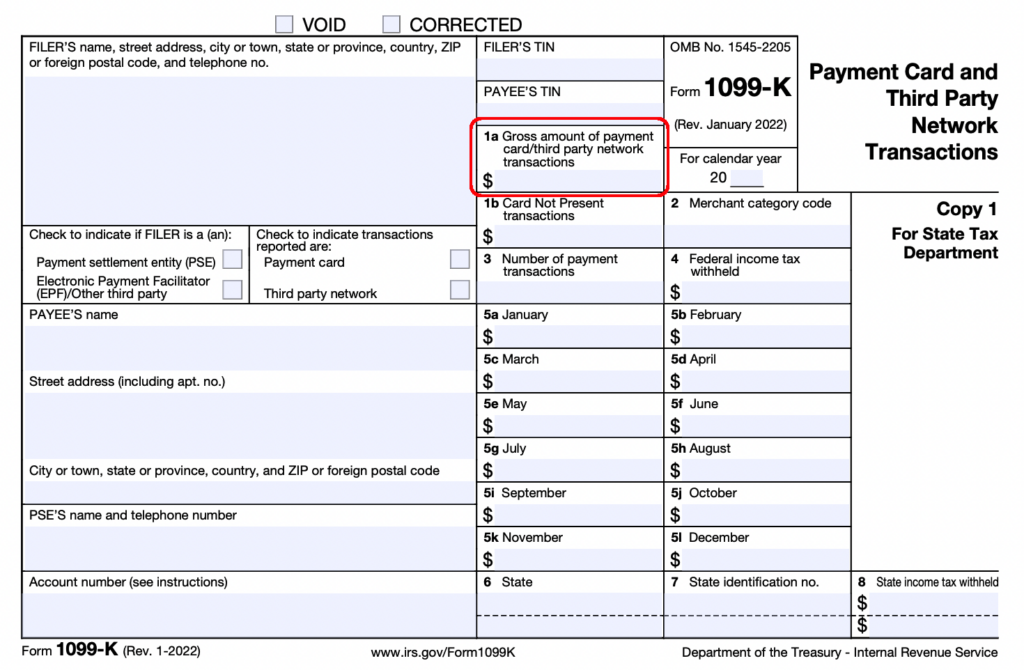

As mentioned earlier, the items you sell on behalf of your consignor do not count as inventory. Then the question becomes, how do you treat those payments? As mentioned in that prior blog post, the most common category we see used is “Commissions & fees.” By making sure each of those payments gets categorized that way, you have legitimate expenses to reduce your taxable income from consignment sales that may show up on your 1099k.

Frequency of payments

The odds are, you don’t want to have to be sending lots of small to midsize payments to a consignor, especially if you start scaling your consignment business. It would be better to keep track of what you owe each consignor and then send them payment on a regular basis when the amount owed hits a certain level. So how do you do that?

Well, it’s pretty easy. The phrase “how much you owe” should provide a clue. We just need to create a new “accounts payable” liability account that will keep track of how much you owe, and then when you pay it.

Automate your eCommerce bookkeeping with Seller Ledger.

Tracking consignment commissions owed

To start, go to the Settings -> Accounts in your Seller Ledger account (or click “Manage accounts” on your Dashboard):

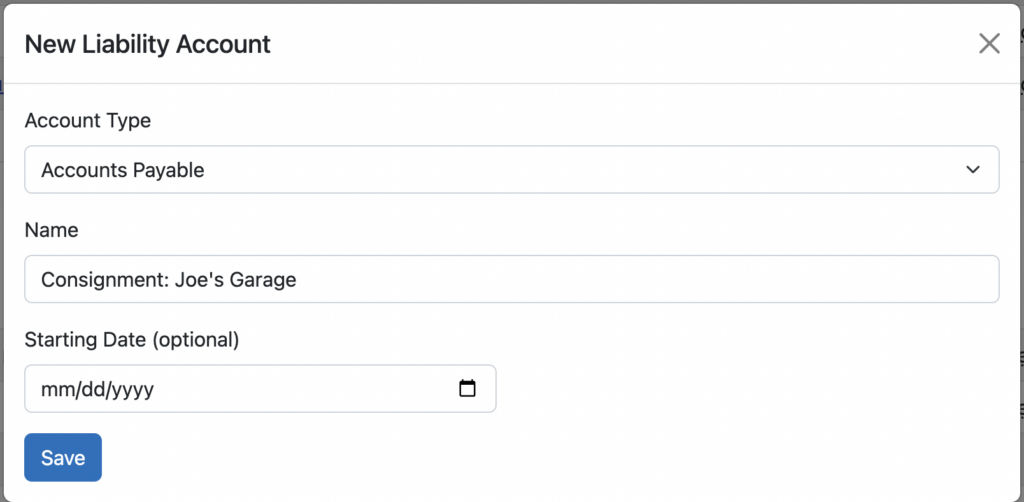

Scroll down the page a bit and click the button to “Add Liability Account.” Then, select “Accounts Payable” as the Account Type, pick a name and, optionally, a start date and opening balance.

If you sell items for more than one consignor, you might think about creating an account for each one of them. But as you’ll see, you can track all of your consignor payments in a single account too.

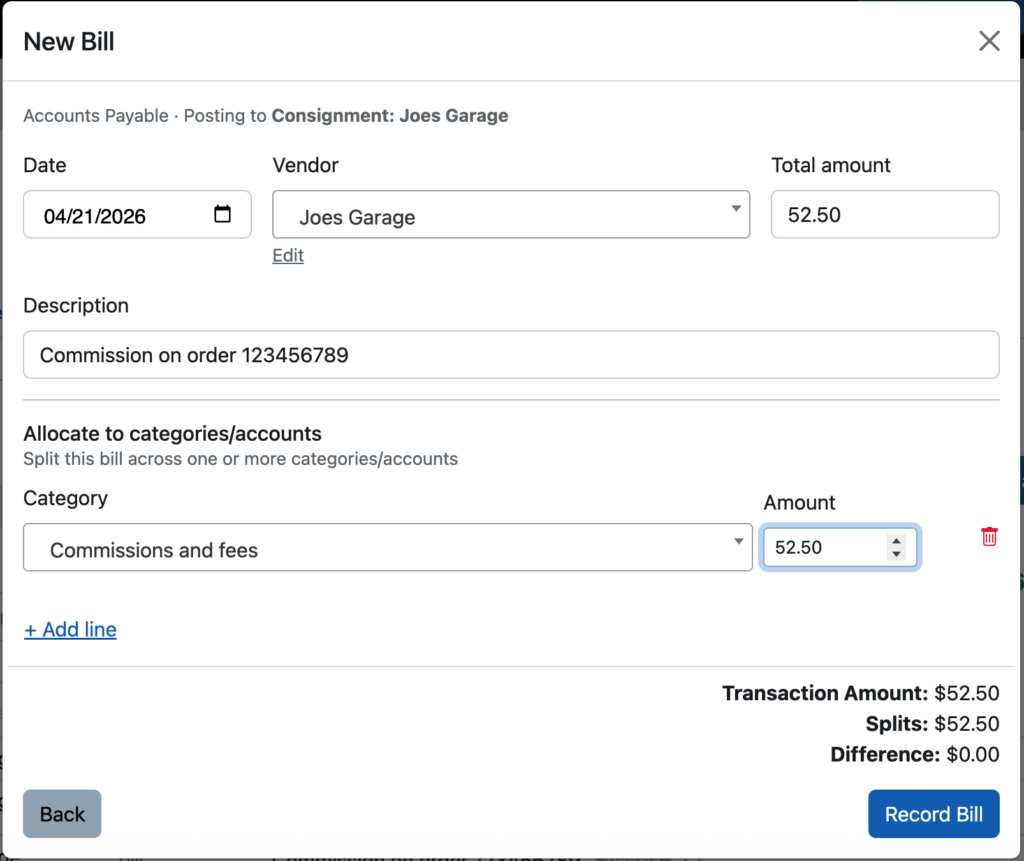

Now that you have created an account for tracking consignment amounts owed, click into it from your Seller Ledger dashboard to see options for recording bills and payments. Each time you have an item sell, and you calculate the commission based on the net profits we outlined earlier, simply click the button to “Record a bill” and enter the details for that commission amount. Don’t forget to categorize the amount owed as “Commission and fees.”

As you sell more items for this consignor, continue to record those commissions within this account. You will see your account balance grow over time:

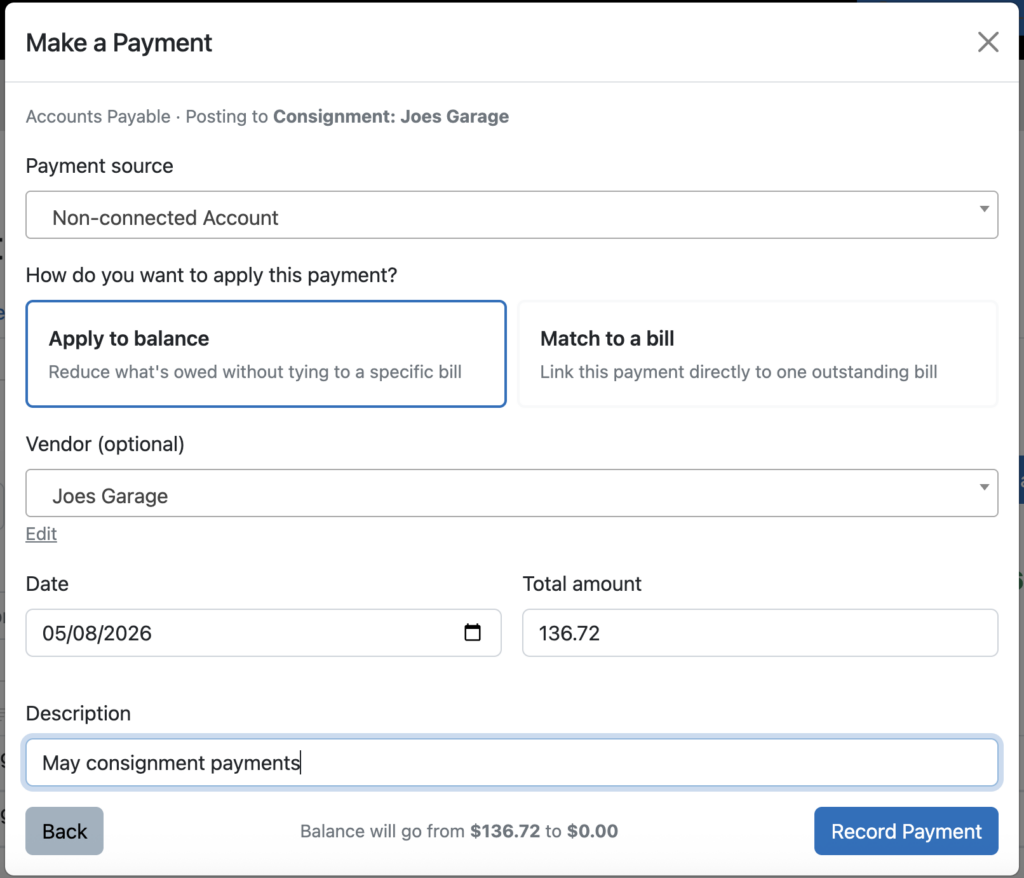

Tracking commission payments

Now, when it comes time to send a payment to your consignor, you have a couple of choices on how to do it. If you have a linked bank account where your payment is imported, you can categorize the payment amount as “Transfer: Consignment: Joes Garage”. Or, if you don’t have a linked bank account, just click into this account, click the “Make a Payment” button, and record the payment details. Because we have multiple commissions to be paid out, we can click the “Apply to balance” option.

Click “Record Payment” and voila – you have paid all of the outstanding money owed to your consignor. And better yet, you get to determine how often you make those payements.

Ready to automate your eCommerce bookkeeping?

Join thousands of sellers who save hours every month with Seller Ledger.

No credit card required