Since we launched, Seller Ledger has automatically imported up to 90 days of transaction history from connected marketplaces, eCommerce platforms, banks and credit cards. This was designed to give everyone a chance to really get to see how the software works for them, on real data, during the 30-day free trial.

However, a number of customers over the years have asked for the ability to choose a specific start date. This has been most prevalent at the beginning of tax years, as customers like to start “fresh” (often after switching from more expensive, more complex solutions:)

Seting your own start date

While Seller Ledger still imports 90 days automatically, it is now super simple to go in and change, on connected-account by connect-account basis, when you would like data to import from.

First, just click on the connected accounts whose import start date you’d like to change:

Next, click on the edit/pencil icon at the top of the account view:

You’ll see a new option to choose a start date. Just pick the start date you’d like:

Click “Save” and you’re all set.

If you had any transactions prior to the new date you’ve entered, they will be deleted from the system. If you don’t want those older transactions deleted, DO NOT set a more current date than you want transactions for.

Billing limitations still apply

If you are just starting a free trial, you won’t be able to enter a date from the start of the prior tax year (or longer.)

What does it mean to track your eBay sales, how should you go about it, and why should you bother to do this?

There are many reasons tracking your eBay sales is valuable. It can help you to understand how much money you are making on your eBay sales. You can better understand all the costs involved, and it will help you to get organized when you have to pay taxes on profits from your eBay sales. Most importantly, it will help you understand whether or not this eBay business is something you should continue to invest your time in and grow.

What to Track for eBay Sales

What are the key things to track for your eBay sales? Youʻll find many of the basic elements in your reports in eBay’s Seller Hub. However, there are a few things you should be tracking and double-checking outside of those standard eBay reports as well. This image shows an overview of the key things to track, and we’ll discuss each of these in more detail.

Sales Price

Often referred to as Revenue, this is the value of your sales that have completed on the eBay platform. To find these numbers on eBay, login to your eBay account. Go to the Seller Hub and click the Performance tab at the top. Select Sales from the left-hand menu and you will see a summary of your recent Sales. You can modify the dates for the report to select the time-period you would like to review.

Included in your Sales Price is any Shipping amount youʻve charged to the buyer as well. This counts as part of your revenue, because itʻs possible you could be making a profit on Shipping charges. If youʻre charging the customer more than your actual costs for shipping, thatʻs profit.

Item Cost

This is how much you paid to acquire the items you have sold. eBay recently released a new feature where you can include “Your Cost” in eBayʻs Seller Hub when listing an item, though many customers donʻt want to share this information with eBay (so that eBay doesnʻt have a full view into their profits.) This value is important to track however, so that you know how much profit you made on your sales. Unless you’ve been selling personal items at a loss, you will need to pay taxes on the profits from your eBay sales at the end of each year.

eBay Fees

These are the fees that eBay charges as a commission on the sale. While they may seem expensive, eBay also delivers a lot of value for these fees. Think of the effort you would have to go to in order to advertise each item for sale on your own. Leveraging eBay’s existing audience that is already searching for what you have to sell takes much less effort. If you want to read more on this topic, check out this blog post about all you get for your eBay fees.

Advertising Fees

In addition to the standard fees that eBay charges, you may have paid additional fees to advertise your listingsand generate increased visibility for them. These fees will also play an important role in your total costs and your profitability. Youʻll subtract both standard eBay fees and eBay Advertising fees from your Sales to calculate your Profit.

Taxes & Government Fees

eBay both collects and remits Sales Tax for your items. Because they are collecting and remitting the same amount for each of your sales, this will not impact your profitability.

Shipping & Handling Costs

You will track shipping costs differently depending on whether you are purchasing your shipping labels through eBay or outside of eBay. If you are purchasing shipping outside of eBay, you may leverage a company like Pirate Ship or Ship Station to do this. In either case, this is an important part of your cost structure to track. If you purchase a shipping label through eBay, the cost of the shipping label will be subtracted from the eBay payout before you receive it. You can view a report in eBay’s Seller Hub to see your total “Shipping Labels”costs for the year. If you purchase your shipping outside of eBay this cost will need to be tracked separately.

The actual postage is one part of your Shipping Costs, but you may have others as well. Purchases of shipping supplies such as boxes, packing tape and bubble wrap are important to document. In addition, if you are driving your packages somewhere be shipped, you may qualify to deduct the mileage for these trips.

Returns and Refunds

When a customer returns an item and you issue a refund back to that customer, it’s important that your eBay Sales Tracking records this transaction as well. Depending on which reports you review on eBay, Returns and Refunds may or may not be included. When you calculate your profit at the end of a year for tax purposes, make sure to subtract out any returns/refunds from your total sales. This is something that can be easily missed (even on the 1099-k forms eBay issues to you). You don’t want to overpay your taxes as a result!

Additional Expenses

As an eBay seller, you will likely have additional expenses that are part of running your eBay business. This might include materials like shelving, bins or garment racks for storage, photography equipment and lighting, and more. We discussed driving packages to the post office above, but you might have other driving expenses as well such as going to a store to source additional inventory. The IRS allows you to deduct mileage expenses for these trips. You may also qualify for the home office deduction if you are using a portion of your home for your eBay business. Track all of these expenses so that you can subtract them from your total sales to pay taxes on the smaller amount that is your true profit.

What are the Best eBay Sales Trackers?

Now that you know all the things you need to track, what is the best way to do this? Weʻll talk through the pros and cons of some different methods below.

eBay Seller Hub Reports

The first place to find basic reports about your eBay Sales is eBay itself and the Performance reports provided in eBayʻs Seller Hub. Youʻll need to be logged into eBay to view these. As we discussed previously however, this is not enough to provide visibility to your full sales and expenses.

Spreadsheets

Many sellers track sales and expenses manually in an Excel spreadsheet when they are first starting out. On the plus side, you can design a spreadsheet to track things exactly as youʻd like to see them. On the minus side, if youʻre selling more than a small volume of goods, this becomes cumbersome very quickly however. Itʻs easy to make mistakes and miss things. To see an example of an eBay Tracking spreadsheet, check out this one from Mark Tew, NotYourDadsCPA, which is available as a free download.

Automated Accounting Software

Automated accounting software can automatically pull in all your data from eBay, including your Sales, Shipping Costs, Fees, Returns and Refunds. While you will have to pay for this software, the time you will save is well worth it if youʻre selling more than a small number of items. If youʻre interested to learn more about how that works, you can read about it here. Companies such as Seller Ledger , Quickbooks and Xero can automate this process for you. This Bookkeeping Guide for eBay Sellers includes a comprehensive review of these solutions with pros and cons of each company.

Why use an eBay Sales Tracker?

Why go to all this effort when eBay has basic reports? If you’re like most eBay sellers, doing the work to review your numbers is not the fun part of running your eBay business. You’d rather be sourcing new items and selling! But it really is worth it to know your numbers, and here are some key reasons to go beyond the basic reports eBay provides.

1. Not all of your costs are captured in eBayʻs reports

As we outlined above, many costs are not captured by eBayʻs reports. The cost of your inventory, your shipping & handling costs (including shipping materials), your mileage expenses and more cannot always be found in an eBay report.

2. Avoid over-paying your taxes

Without capturing ALL of your costs, you are likely to overpay your taxes at the end of the year. Even eBayʻs 1099-k reports donʻt always include all the returns are refunds that have been issued, so they may overstate your sales. Without your full set of costs, they will overstate the amount of profit you need to pay taxes on. This is real money weʻre talking about! Donʻt pay more than you need to!

3. Understand your Net Profit per Order

Once you are tracking all of your income and expenses, you can get an understanding of your Net Profit per Order. This allows you to see which of your items are making you the most money. Once you know that, you know what you want to source more of and what you want to stop selling because youʻre losing money on it. This is how you can improve the profitability of your eBay business over time.

4. Scale your eBay Business with Confidence

Once you truly undertsand how much money you are making, you can have the confidence to go out there and grow your business! Aquire the right inventory and sell more so that your eBay Sales can be more than just a small side hustle and turn into a real source of income for you.

We hope youʻve found this article helpful. Find more articles about tracking your eBay business on the Seller Ledger blog, or try Seller Ledgerʻs 30 day free trial to automate your eBay Sales Tracking today.

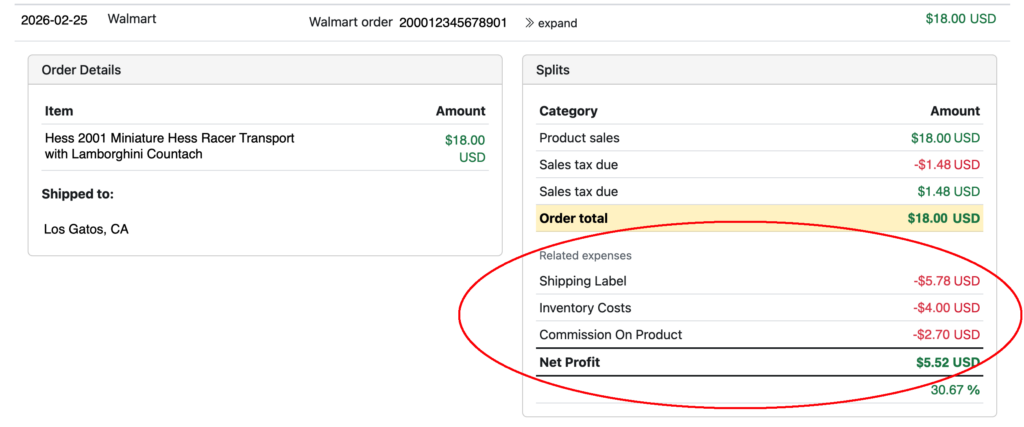

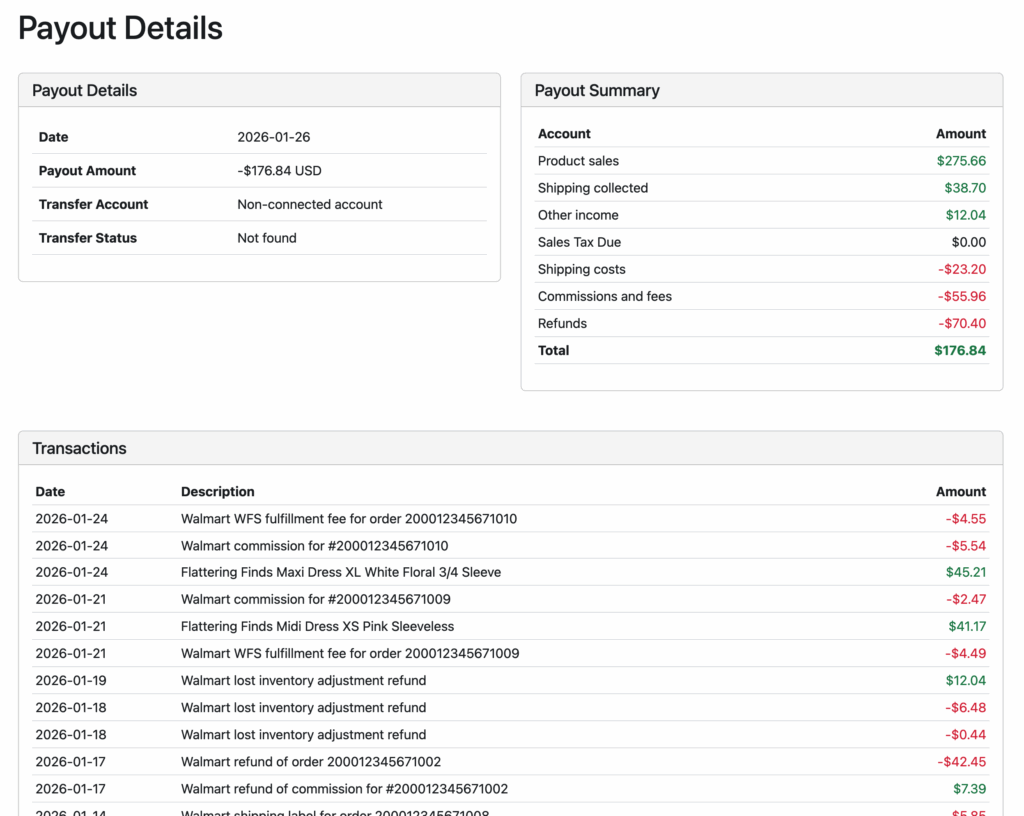

As we have done with both eBay and Amazon, we also recently released the ability for Walmart customers to view the NET profit on each order.

Walmart profit per order

Click the “>>expand” link next to any order in your Walmart account. Under the category split totals that make up that order, you will see a new “related expenses” section that includes other fees and expenses that are tied to that order. This includes the Walmart commission charged for that order. In addition, if you purchase shipping labels through Walmart, we include that too.

Lastly, as mentioned when rolling out our Gross Profit report, if you track your inventory costs at the item level and use unique SKUs for each of your Walmart items, we will match those costs to the correct item. That, plus the other related expenses, helps you see the true NET profit for each order on Walmart.

If you are a Walmart seller who’d like this kind of visibility and automation in your accounting, give Seller Ledger a try. We offer a 30-day free trial, no credit card required.

While we have alluded to this in other posts, a question from a customer reminded us that we could be more explicit about sales tax and Etsy.

In a nutshell, as a marketplace facilitator, Etsy takes on the responsibility of both collecting sales tax from buyers and remitting it to the state. But, those amounts do show up in your Etsy transactions. So how does one account for them?

Sales tax is a liability…not income or expense

When sales tax is collected from a customer, it is not considered income. It becomes a “liability”, accounting jargon for “owing money to someone else.” In this case, it is money owed to the state. And that is how Seller Ledger treats the sales tax that is collected. It becomes money you owe to the state. When Etsy remits that money to the state, the “liability” gets offset.

This means that sales tax will not impact your profit and loss total, which determines your income tax owed.

How Etsy reports sales tax

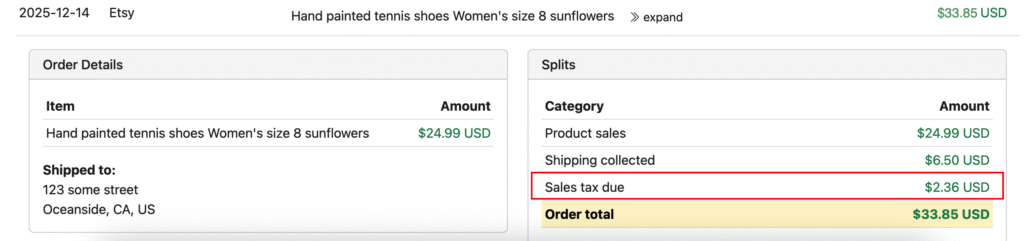

Here’s where it gets a bit interesting. Other marketplaces, like eBay and Amazon, indicate that sales tax is both collected and remitted on the order. In those cases, Seller Ledger creates entries for both the sales tax collected and the sales tax paid, right in the order itself. That means that sales tax does not impact the order total, because anything collected is also subtracted out.

Etsy, on the other hand, includes sales tax in the total order amount. For example, if you click into your Etsy account from your Seller Ledger dashboard, and expand an order where sales tax was collected, you’ll see something like the following:

Notice that the total amount of the order includes the sales tax collected.

It turns out that Etsy then provides a separate transaction for the sales tax remitted. As you can see above this order, there is a separate remittance transaction for the same amount.

As we mentioned before, this doesn’t impact your profit and loss one way of the other. But it can make it harder to reconcile numbers from different places, especially when 1099s come out. And if you’re interesting in more potentials sources of confusion on Etsy numbers, check out this post.

While we’ve had this functionality around for a while, a recent customer email reminded us that we can always do a better job explaining how things work.

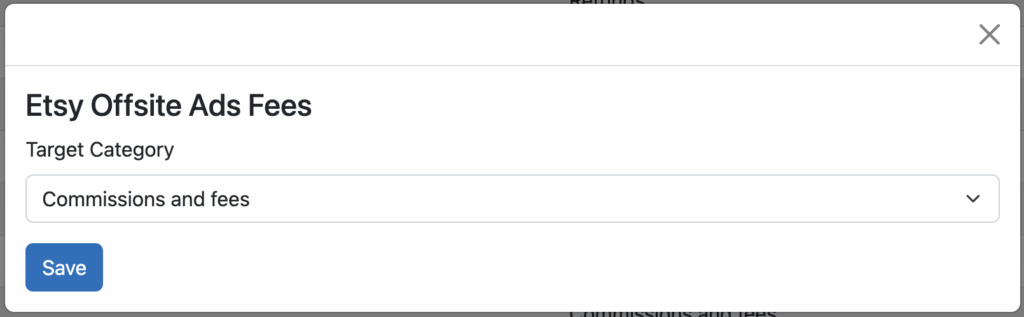

In this case, an Etsy seller wrote in and asked how she can change the category on Etsy ads from the default of “Commissions & fees” to “Advertising. And she’s not the first customer to ask this.

Fortunately, Seller Ledger makes it quit easy to make that change. Simply go to the Settings tab and click the “Customize” sub-tab. If will bring you to a screen that looks like this:

You’ll notice that there are a lot of different Etsy fees, including:

Generic fees

Listing fees

Prolist fees

Renew fees

Renew expired fees

Renew sold auto fees

Renew sold fees

Renew auto expired fees

Payment processing fees

Offsite ads fees

Transaction fees

Shipping transaction fees

Shipping label insurance fees

If, as our customer was asking, you wanted to categorize Offsite ad fees as “Advertising”, just click on the edit/pencil icon on the far right to be given this screen:

Then just change the category to “Advertising”, click the “Save” button and you’re all set. Seller Ledger will treat all of these transactions as “Advertising.” This applies not only to all future transactions, but all prior transactions.

What about regular Etsy Ads?

Unfortunately, Etsy does not make the fees for their “on site” ads available through their API. Learn how to handle them here.

Pro tip

You may wish to group some of these Etsy fees into more granular categories. For that, we recommend creating sub-categories, and then mapping these details fees to those sub-categories.

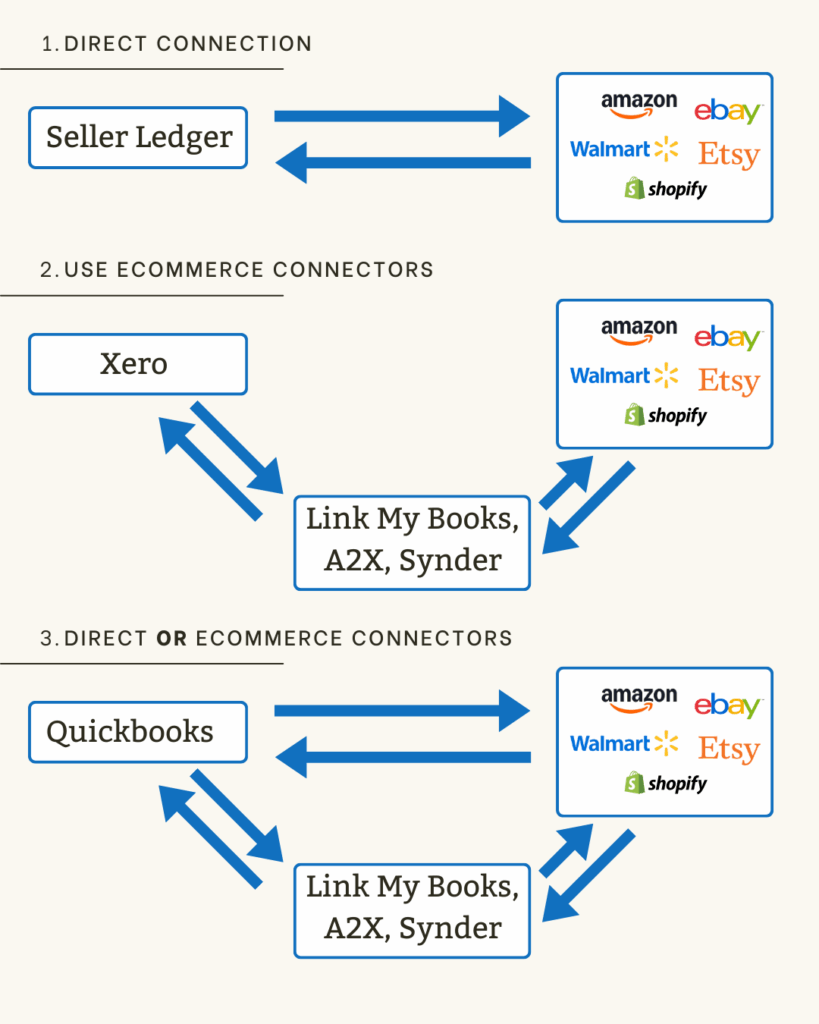

This article will explain how accounting software providers receive eCommerce data, how safe it is for sellers to use, and how to think about choosing which provider to go with if you want to automate your eCommerce accounting.

Accounting Software providers such as QuickBooks, Xero and Seller Ledger use something called an API to import eCommerce sales data from online marketplaces such as Amazon, eBay, Walmart and Etsy. API stands for “Application Programming Interface.” They have been in existence for decades, and they are safely used all over the internet.

How Do API’s work?

Think of an API as a private way for software programs to talk directly to each other and exchange information. In addition to providing a standardized way to exchange data, most uses of APIs also include permissions to manage customer data privacy and security.

In the case of accounting software getting information from online marketplaces, the first step is for the accounting software to get approved as a reliable partner. The large marketplaces, with tons of customer data, don’t want just any software accessing their data. Once approved, each accounting software is issued what’s effectively a digital ID, which they can use to identify themselves each time they request information.

The next major step is making sure that the accounting software actually has permission to get data on behalf of an actual customer. In order to get this permission, the accounting software sends the customer to a special page to let the marketplace know what data they are permitted to share. This happens on the marketplace’s website, so no passwords are exchanged. Once the user gives permission, the marketplace sends the accounting software a token that can be used in future requests for data. Think of that token as a permission slip that the accounting software presents each time it asks for data.

Do all software providers connect with marketplace API’s in the same way?

We’re glad you asked! No, they do not. This is one of the big differences in the various accounting software solutions for eCommerce sellers. Some accounting software companies connect directly to the marketplaces, others require the use of 3rd party eCommerce connectors like A2X Accounting, Link My Books and Synder. And some choose to offer both.

Below is a diagram showing the various options used by leading eCommerce accounting platforms.

Let’s talk about some of the advantages and disadvantages of each option:

Simplicity: Fewer moving parts means less work getting set up. And the connections and data are built into the core parts of the accounting software.

Lower costs: You don’t have to pay for extra software subscriptions.

Accountability: When marketplaces change their data, or introduce new fees, there’s only one party responsible for updating the software.

Cons

Less flexible: If your accounting needs are more unique, having the ability to choose between different methods of data connection (e.g. detailed vs summary) could be valuable.

3rd Party eCommerce connectors

Using 3rd party eCommerce connectors basically means an accounting platform is outsourcing the eCommerce data collection and classification to someone else. These 3rd parties specialize in eCommerce connectivity, so it’s a legitimate way to delegate responsibility. Xero has taken this approach.

Pros

Expertise of 3rd party connectors: The leading providers have been working with eCommerce Marketplaces for year, and are very familiar with the data.

Keeps books “clean and lean”: By delegating the task of collecting and summarizing eCommerce data, you can reduce the likelihood that your traditional accounting software gets bogged down by data it was never designed to handle.

Cons

Complexity: By using what some call “middleware”, you will have more setup to get things working as desired. And because the eCommerce connections are not baked into the core product, the user experience may feel disjointed.

Cost: Needing to use a separate software system will invariably cost more.

Choice of Direct OR 3rd part connectors

Then there’s the option for maximum flexibility. Some accounting platforms build their own direct connections to leading eCommerce marketplaces, but also allow you to choose a 3rd party connection instead. Quickbooks offers this choice.

Pros

Flexibility: You can choose which option works best for your business, even doing it on a marketplace by marketplace basis if so desired.

Experience: In the case of using 3rd party connectors, these tools have been used together for many years by many sellers.

Cons

Quality and coverage: Based on online commentary, there may be issues with how well the direct connection tools are managed. And Quickbooks, as of the time of this post, only provides a limited set of direct integrations (e.g. they don’t connect directly to Walmart.) As such, you could end up with a “kitchen sink” approach.

Cost: If you use a 3rd party connector in addition to a multi-channel tier of Quickbooks, prices could get up there.

Conclusion

As with any decision, your choice of accounting software to use for your eCommerce business comes down to the needs of your business and your personal preference. But, regardless of which option you choose, feel confident that there lots of ways to automate your eCommerce accounting using accounting software.

When we first launched our Whatnot integration, the only sales data available to Whatnot sellers was their Ledger history. Customers could download those reports and then upload the CSV-formatted files to Seller Ledger. Since then, Whatnot has added weekly order reports, which provides much more transaction detail, including:

Item prices

Coupon costs

Shipping costs

Commission fees

Payment processing fees

To take advantage of that, Seller Ledger has rolled out new functionality to automate Whatnot accounting. Customers no longer need to download files from Whatnot and upload them to Seller Ledger. All of that is taken care of.

How to automate your Whatnot accounting

In order to fully automate your Whatnot account within Seller Ledger, you only need two things:

1. You should use the Chrome browser when accessing Seller Ledger so that you can also make use of the second tool (below.)

2. Once you are using Chrome, you will want to install Seller Ledger’s custom-built Browser Extension. This extension allows Seller Ledger to automatically pull down and import the proper transaction details.

They say imitation is the sincerest form of flattery. Well, here’s another form of flattery, though perhaps less sincere. We discovered yesterday that Quickbooks is buying google ads against our product name.

We take that as a compliment, because it must mean that they would like to reach prospective eCommerce customers who are searching for us. That is quite flattering, considering they are:

Significantly larger than our company

Have been around a lot longer than us

Have had years (decades?) to try to enhance their software in ways that would make it work well for online sellers.

Spending on advertising is a lot easier that simplifying an existing product that isn’t particularly well-suited to eCommerce. And we have faith that word will continue to spread about how much better Seller Ledger is for eCommerce accounting.

So we welcome the challenge – the challenge of competing with Quickbooks:)

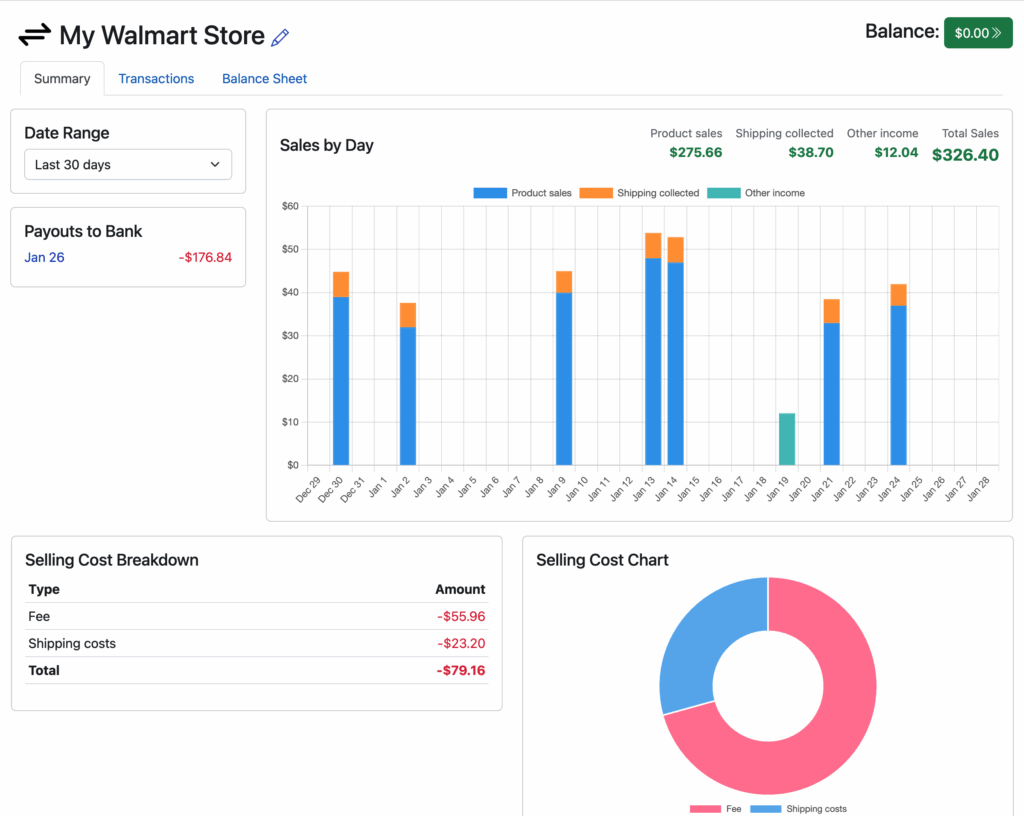

Continuing the work with did for both Amazon and eBay, we’ve just rolled out a new channel summary page for Walmart. While Seller Ledger has been importing Walmart sales, refunds and fees for more than a year now, we’ve made it even easier to make sense of all of that detailed data.

From your Seller Ledger dashboard, just click into your Walmart account to view a screen like the following:

You can choose from a number of date ranges to see your data. You can click into any payout to view a summary of (and mini profit and loss statement for) that payout. You can even drill down to see every single transaction that makes up each payout.

You can also see a summary of your sales and expenses for the period, with a breakdown among selling costs.

Whether you’re thinking of switching or just getting started, this step-by-step guide will help you choose the right solution for your Amazon business.

Amazon (and eCommerce) accounting comes with a rather unique set of challenges, above and beyond traditional business accounting. In addition to regular income and expense tracking, you can expect to face:

Lots of order transactions (if you’re lucky)

Even more fee transactions

Inventory and cost of goods sold tracking

Reconciling platform payouts vs your bank

The good news is, with modern software, you can shrink the time you spend on accounting for your Amazon business from hours a month to minutes.

How do I choose?

First, let’s assume that you’d like to get your Amazon data into your accounting software with as little customization and setup as possible. That will rule out platforms like Wave Accounting and Freshbooks, which not only don’t have direct integrations with Amazon, but they require using a general purpose API (application programming interface) tool like Zapier to make it work. That’s a non-starter for most sellers.

Next, the key question becomes – how much (and what kind of) Amazon data do you want to bring into your accounting software. Specifically, do you want all of the transactions from Amazon or just summarized information?

Detailed vs Summarized Amazon Data

So what does it mean, to get detailed vs summarized Amazon data? Let’s take a look at each method:

Detailed transaction data

This means pulling in every order, including line items, discounts, sales tax collected and remitted, shipping collected and fees subtracted. It also means bringing in shipping label transactions, and LOTS of other Amazon fees.

What are the pros and cons of this approach?

Pros:

You get a perfect understanding of your Amazon accounting, not only at the P&L and balance sheet level, but also down to the net profit on every sale (if your solution can pull that off – more on this later.)

You can automate inventory and cost of goods calculations by mapping sales back to the original inventory purchases.

You avoid the issue of payouts that can span different periods (e.g. an early January payout that includes both December and January transactions.)

Cons:

A lot of folks (especially old-school CPAs) worry about “cluttering up” your books with too much detail, which can bog down your accounting platform’s performance. Amazon does produce an enormous number of small transactions.

Reconciling all of those transactions to the payouts and deposits to your bank can be a royal pain in the neck if your solution doesn’t do this for you (again, more on this later.)

Summarized data

Using this approach, instead of bringing in all Amazon transactions, you summarize them outside of your accounting platform, and instead, match the totals to each payout that shows up in your bank account.

The pros and cons of this approach are pretty much the reverse of the above:

Pros:

Reconciliation of all of those Amazon transaction totals to your payouts should be easier.

You avoid “cluttering up” your accounting software with details you may never need to dig into.

The performance of your accounting software remains high by limiting the data you add.

Cons:

You miss out of net profit calculations.

You can’t automate inventory/cost of goods calculations.

Payouts that span multiple months or years are still problematic.

Biased perspective

We’d like to take a quick moment to point out the following observations. We believe two of the most commonly referenced reasons for choosing the “summarized” approach stems from folks dealing with practical limitations of existing solutions.

First, the idea that a lot of data will “clutter up” accounting software is more a reflection of the design of that software than the data itself. Good software design, especially around the user interface, can do an awful lot to hide details until you’re ready to look for them. In addition, when a software solution already has a lot of non-eCommerce features that already “clutter up” the interface, perhaps avoiding those unused features would help.

Second, the argument about performance is equally fascinating. There are many other platforms that process exponentially more data than accounting platforms and yet are still performant. Just ask Google, Amazon, eBay and Shopify (or TaxJar.) So changing your desired behavior because of the scaling limitations of a platform seems suboptimal.

What are the best options?

In addition to looking at the data options from Amazon, you may have some other criteria specific to you and your business. How much do you want to do yourself vs outsource to an accountant or bookkeeper? Do you want something specifically designed for eCommerce? How much do you value simplicity? Are you price conscious?

We’ll go through the leading contenders in the space, based on current (2026) sentiment:

Seller Ledger

Seller Ledger is one of the newer players in the space, created by several of the original team members behind Outright/GoDaddy Bookkeeping and TaxJar. It provides both the accounting platform plus a direct Amazon integration (as well as many others) and chooses the “detailed transactions” approach.

Seller Ledger is specifically designed for eCommerce sellers, so it has a much simpler user interface and setup process that traditional accounting software. It also has a pricing model that starts much lower and grows with the size of your businesses. Additionally, it does not limit features based on pricing tiers.

Detailed transaction approach

Seller Ledger pulls in all transaction data from Amazon via a custom-built integration. It does not require any third party connectors. And while it does pull in every Amazon transaction, it also ties every single transaction to each payout, and matches those payouts directly to your bank account deposit. This addresses the concerns about payout reconciliation, because it is built into the system, and also avoids the timing issue when a payout occurs around the end of a period.

It groups all transactions related to each Amazon order (including fees, shipping labels, etc) so you can see your net profit per order. That includes cost of goods sold, if you are using unique SKUs. Plus, it can automate inventory levels using the FIFO (first-in, first-out) method.

If you want to outsource your Amazon accounting completely, you can use Seller Ledger and invite your accounting pro to access your data. But bookkeeping services are not included in the price of the software.

Plans start as low as $10/mo for very small sellers and go up based on monthly transaction volume.

Limitations/concerns

As of the time of this writing, Seller Ledger is primarily designed for US eCommerce sellers. It handles US income and sales tax very well, but does not yet provide currency conversion. All non-US transactions are shown and summarized in their native currencies.

It is also exclusively designed for eCommerce businesses, so if you require invoicing other features for service-based businesses, you may want to look elsewhere.

Quickbooks Online or Xero + third party connector

The most familiar names in accounting software, these two classic platforms support all kinds of business types, not just Amazon businesses.

Quickbooks is by far the most popular accounting platform in the market. It has a direct integration option with Amazon, though most commentary suggests using a third party connector (A2X, Link My Books, Synder) to properly handle Amazon data. It is also more recommended for US-based businesses. However, Quickbooks is also relatively expensive and is notorious for raising prices (as in, up 35% in the last 3 years as of this writing.)

Xero has no direct integration with Amazon, relying instead on those same third party connectors. It tends to be much more recommended for non-US businesses (especially anyone based in New Zealand or Australia.) And it is quite a bit less expensive than Quickbooks.

Now let’s look at the third party connectors. While there are a lot of more general purpose middleware solutions out there (e.g. Zapier, Webgility, etc,) we are going to focus on the 3 that appear to be the best tailored for eCommerce.

A2X Accounting is well respected for their data accuracy and working especially well with Quickbooks. They use the “summarized” approach to bringing in Amazon data, though they have a creative solution for splitting payouts across periods. They are said to be a bit more complex than other solutions, and more expensive.

Link My Books, which also uses the “summarized” data approach, focuses a bit more on ease of use and VAT compliance. It is also a bit less expensive that A2X Accounting.

Synder is a more broad-based connector, working not only with Amazon and other marketplaces, but also with payment platforms like Stripe, PayPal and Square. They also support the “detailed” approach to Amazon data in your accounting platform. They tend to me a bit more complex, which, given their extra capabilities makes sense. And their pricing is a bit higher.

The combos

Given the performance and “clutter” concerns, and seeing the US vs non-US focuses, it would seem like the choices really come down to:

Quickbooks + A2X Accounting (if you are US-based)

Xero + Link My Books (for non-US businesses.)

In both cases, you will be using the “summarized” Amazon data approach, with the pros and cons mentioned earlier.

Both combinations are also designed very well to worth with accounting professionals.

In terms of pricing, Quickbooks Online + A2X Accounting is going to be on the more expensive side, at likely $100-$200/mo to start (depending on how many channels you link and transactions you process.)

Xero + Link My Books appears to start at about half that rate and go up from there.

One additional thought: by using two different applications, it might make for fun customer support inquiries if/when something changes or breaks. And given how often Amazon adds or changes their fees, software updates are inevitable.

Finaloop

Another relatively new option, Finaloop is a “full service” solution for eCommerce businesses looking for software + bookkeeping all in one place. Like Seller Ledger, they provide the accounting platform and a direct integration with Amazon, using the “detailed” data approach. And similar to Synder, they also link to other marketplaces and payment platforms. But their big claim to fame is that their service also comes with team members who will do your bookkeeping for you.

With pricing that starts at $250/mo, the base pricing isn’t that much more expensive than Quickbooks + A2X Accounting. But, prices rise pretty quickly and are based on your business revenue.

Limitations/concerns

Given what happened to Bench Accounting, another startup that tried to build a “software + bookkeeping” business (more broadly than eCommerce,) you’ll want to make sure you can take your data with you if needed.

Summary Comparison

Seller Ledger

Best for:

Small to mid-sized Amazon sellers in the US

Those who want detailed Amazon data

Those who want an affordable option

Quickbooks + A2X Accounting

Best for:

Scaling US-based Amazon sellers

Those who want summary level data

Those willing to pay for quality/reputation

Already have an accounting pro that likes this combination

Xero + Link My Books

Best for:

Scaling non-US based Amazon sellers

Those who want summary data

Those looking for a more affordable summary solution

Already have an accounting pro that likes this combination

Finaloop

Best for:

Amazon sellers who want to outsource their bookkeeping but don’t already have an accounting pro