Cash-based Inventory tracking

A.k.a “The simplest way to calculate cost of goods sold”

There’s a lot of content out there on the internet around inventory, accounting, cost of goods sold and taxes. While it has the potential to be very confusing, we’re going to try to simplify things a bit, especially for small online sellers.

Definitions

The most basic definition of cash-based inventory tracking (versus accrual accounting for inventory) is as follows.

Cash-based

Expense the cost of your inventory when you buy it, regardless of when it sells

Accrual

Expense the cost of your inventory when it sells, regardless of when you bought it

Historically, the IRS pushed most people to use the accrual approach, even if using cash-based accounting for the rest of the business. But we have seen a TON of sellers file this way, and know that some tax pros have dug into this as a legitimate approach. I don’t want to get into any tax advice here, but I will show you how, practically, each approach works, and how they can actually be very, very similar to each other.

Let’s take a look at how you can used cash-based inventory tracking using Seller Ledger. This is actually the default setting when you first start using Seller Ledger. It works by giving you the option to categorize expenses as “cost of goods sold” when you purchase them and deduct the total amount on your tax return. Check out this video tutorial on expensing cost of goods sold to see exactly how that works.

This is the simplest approach you can take. But I want to explain what you’re effectively doing if you file this way.

Understanding the math

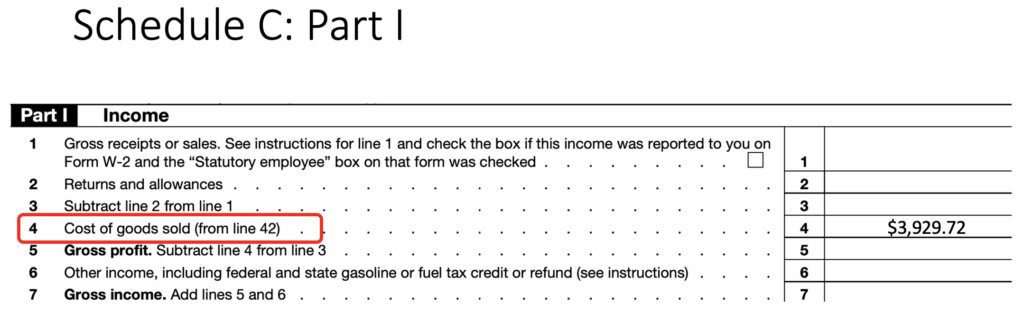

If you look at the actual Schedule C form provided by the IRS, yes, line 4 (highlighted in red) does ask for Cost of Goods Sold. But in parentheses, it says “from line 42”. Line 42 comes from Section III.

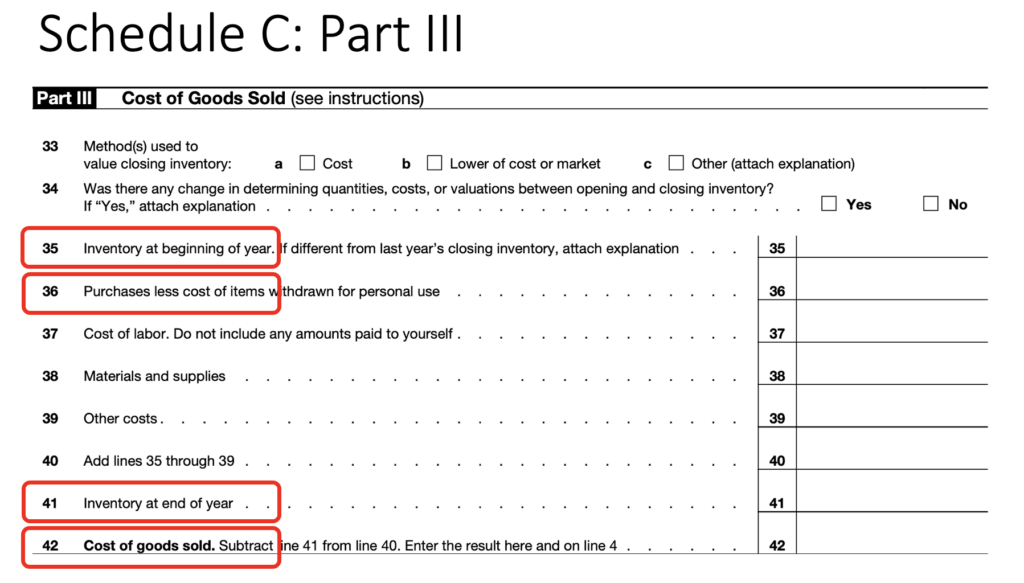

Here is what Section III of the Schedule C looks like:

The key lines in Section 3 (again, highlighted in red) are Lines 35 (your beginning of year inventory), 36 (the cost of items you purchased throughout the year) and 41 (your end of year inventory.)

As you can see, Cost of Goods is calculated using this basic formula, which we can lay out in a slightly different way:

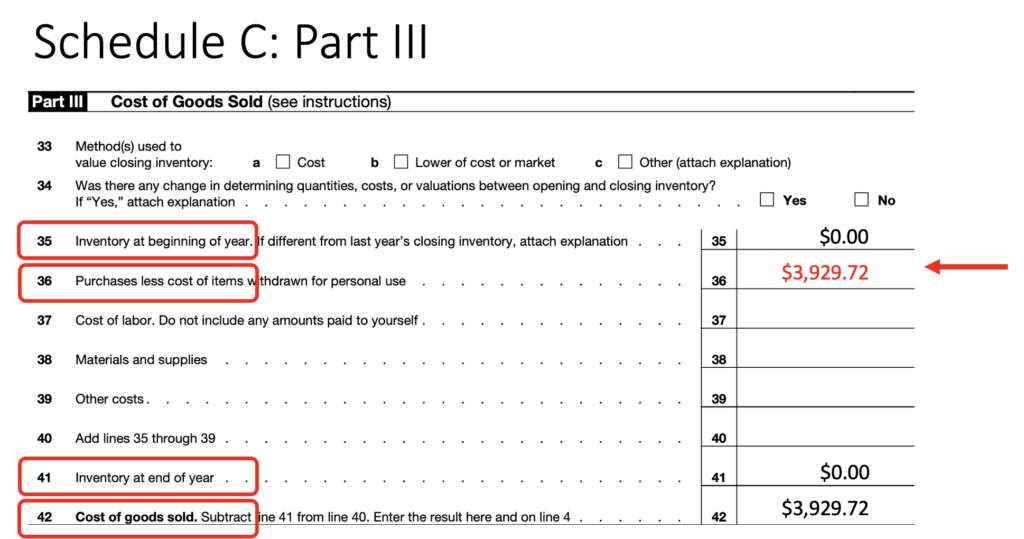

By simply categorizing all of your purchases as cost of goods sold, you’re basically saying to the IRS, everything I bought, I sold within the same year. As in, if this is my first year selling, my beginning inventory was zero (because I didn’t buy anything the prior year) and my ending inventory is zero, because I’ve sold everything I bought this year. Now, using that same formula above, you would get:

In our example, you’d be declaring a starting inventory balance of $0 and an ending inventory balance of $0. In order for your costs of goods sold to end up at $3,929.72, you would enter that same amount under items purchased for the year.

The only thing that is changing is that, instead of calculating Cost of Goods Sold based on the other 3 values, you are backing into the Purchases value by assuming that opening and ending inventory is zero. That’s all the Cash-method for inventory and cost of goods sold tracking is. In fact, we’ve seen cases where tax professionals are filing returns using a pretty significant, non-zero opening and matching closing inventory balance, and still just declaring that purchases and cost of goods sold are the same.

In fact, the funny secret here is that, for all intents and purposes, cash-based inventory (a.k.a. just writing off your purchases as you make them,) is no different than periodic (or, as well call it, “balance-level”) accrual inventory tracking. The only difference? Whether you actually count up the cost of your unsold inventory at least once a year.

A big limitation

All of the above is meant to outline the easiest way to track inventory for tax purposes. But, the cash-based method for inventory tracking (as well as the periodic/account-level method of accrual accounting) do have a pretty big limitation – they won’t help you figure out how much money you make on each sale or type of product. For that, you are going to want to look into tracking at the item-level (a.k.a. continuous inventory management.)

If you are an eCommerce merchant who wants to keep bookkeeping simple, we strongly recommend giving Seller Ledger a try. We connect directly to LOTS of leading marketplaces and platforms, as well as most banks and credit cards. You can try us for free for 30 days, no credit card required.