Best Amazon Accounting Software for 2026

Whether you’re thinking of switching or just getting started, this step-by-step guide will help you choose the right solution for your Amazon business.

Amazon (and eCommerce) accounting comes with a rather unique set of challenges, above and beyond traditional business accounting. In addition to regular income and expense tracking, you can expect to face:

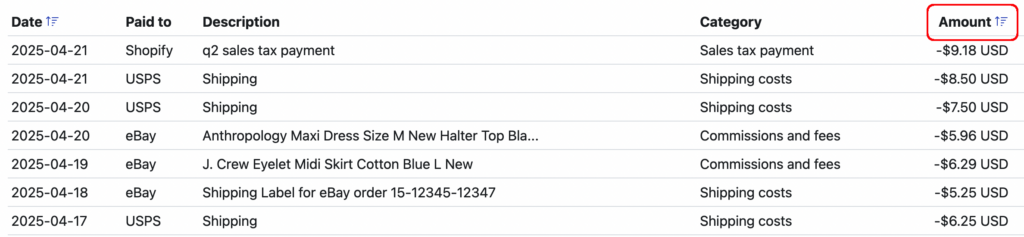

- Lots of order transactions (if you’re lucky)

- Even more fee transactions

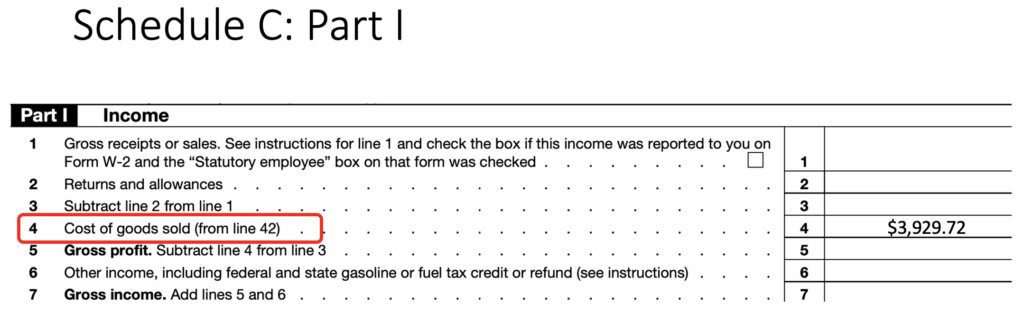

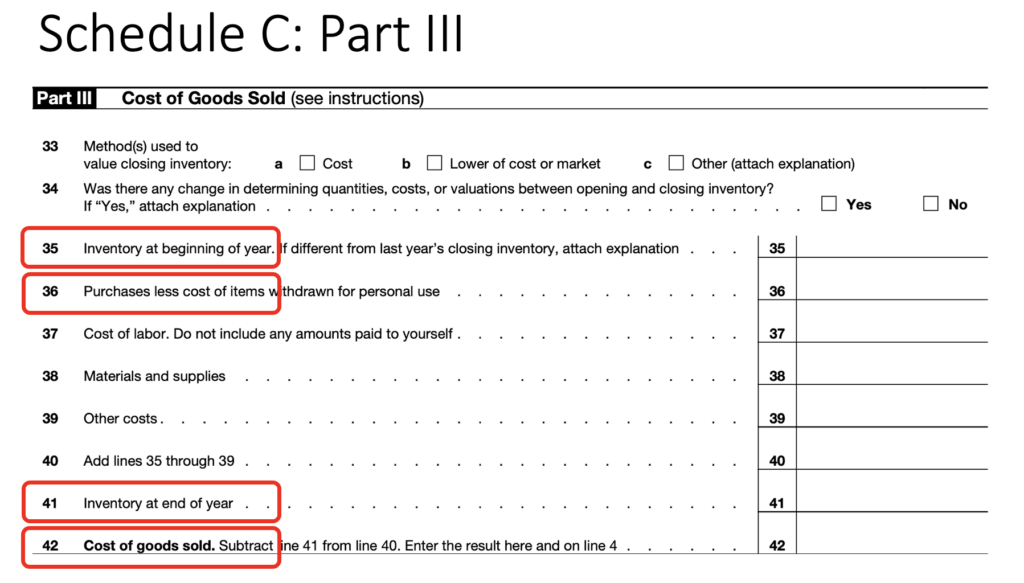

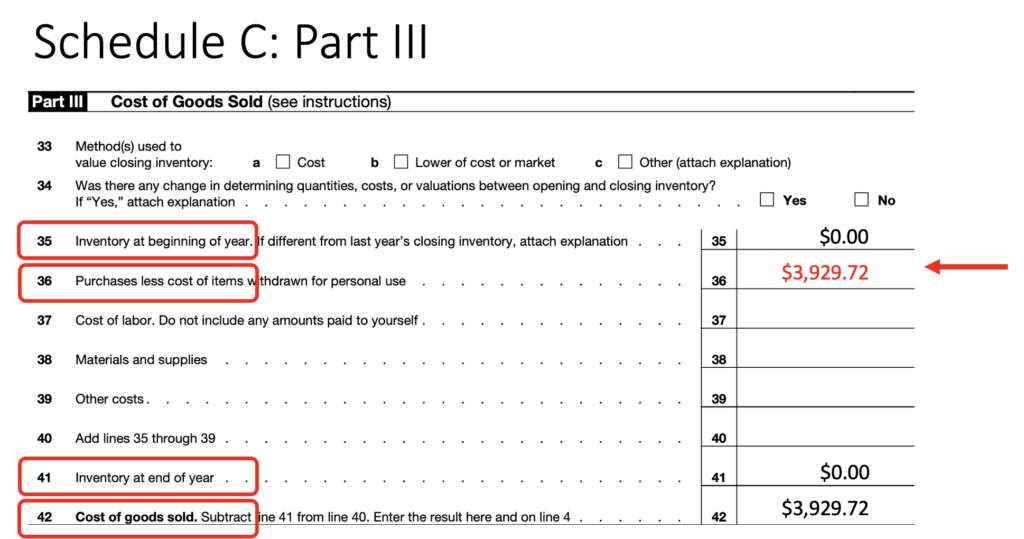

- Inventory and cost of goods sold tracking

- Reconciling platform payouts vs your bank

The good news is, with modern software, you can shrink the time you spend on accounting for your Amazon business from hours a month to minutes.

How do I choose?

First, let’s assume that you’d like to get your Amazon data into your accounting software with as little customization and setup as possible. That will rule out platforms like Wave Accounting and Freshbooks, which not only don’t have direct integrations with Amazon, but they require using a general purpose API (application programming interface) tool like Zapier to make it work. That’s a non-starter for most sellers.

Next, the key question becomes – how much (and what kind of) Amazon data do you want to bring into your accounting software. Specifically, do you want all of the transactions from Amazon or just summarized information?

Detailed vs Summarized Amazon Data

So what does it mean, to get detailed vs summarized Amazon data? Let’s take a look at each method:

Detailed transaction data

This means pulling in every order, including line items, discounts, sales tax collected and remitted, shipping collected and fees subtracted. It also means bringing in shipping label transactions, and LOTS of other Amazon fees.

What are the pros and cons of this approach?

Pros:

- You get a perfect understanding of your Amazon accounting, not only at the P&L and balance sheet level, but also down to the net profit on every sale (if your solution can pull that off – more on this later.)

- You can automate inventory and cost of goods calculations by mapping sales back to the original inventory purchases.

- You avoid the issue of payouts that can span different periods (e.g. an early January payout that includes both December and January transactions.)

Cons:

- A lot of folks (especially old-school CPAs) worry about “cluttering up” your books with too much detail, which can bog down your accounting platform’s performance. Amazon does produce an enormous number of small transactions.

- Reconciling all of those transactions to the payouts and deposits to your bank can be a royal pain in the neck if your solution doesn’t do this for you (again, more on this later.)

Summarized data

Using this approach, instead of bringing in all Amazon transactions, you summarize them outside of your accounting platform, and instead, match the totals to each payout that shows up in your bank account.

The pros and cons of this approach are pretty much the reverse of the above:

Pros:

- Reconciliation of all of those Amazon transaction totals to your payouts should be easier.

- You avoid “cluttering up” your accounting software with details you may never need to dig into.

- The performance of your accounting software remains high by limiting the data you add.

Cons:

- You miss out of net profit calculations.

- You can’t automate inventory/cost of goods calculations.

- Payouts that span multiple months or years are still problematic.

Biased perspective

We’d like to take a quick moment to point out the following observations. We believe two of the most commonly referenced reasons for choosing the “summarized” approach stems from folks dealing with practical limitations of existing solutions.

First, the idea that a lot of data will “clutter up” accounting software is more a reflection of the design of that software than the data itself. Good software design, especially around the user interface, can do an awful lot to hide details until you’re ready to look for them. In addition, when a software solution already has a lot of non-eCommerce features that already “clutter up” the interface, perhaps avoiding those unused features would help.

Second, the argument about performance is equally fascinating. There are many other platforms that process exponentially more data than accounting platforms and yet are still performant. Just ask Google, Amazon, eBay and Shopify (or TaxJar.) So changing your desired behavior because of the scaling limitations of a platform seems suboptimal.

What are the best options?

In addition to looking at the data options from Amazon, you may have some other criteria specific to you and your business. How much do you want to do yourself vs outsource to an accountant or bookkeeper? Do you want something specifically designed for eCommerce? How much do you value simplicity? Are you price conscious?

We’ll go through the leading contenders in the space, based on current (2026) sentiment:

Seller Ledger

Seller Ledger is one of the newer players in the space, created by several of the original team members behind Outright/GoDaddy Bookkeeping and TaxJar. It provides both the accounting platform plus a direct Amazon integration (as well as many others) and chooses the “detailed transactions” approach.

Seller Ledger is specifically designed for eCommerce sellers, so it has a much simpler user interface and setup process that traditional accounting software. It also has a pricing model that starts much lower and grows with the size of your businesses. Additionally, it does not limit features based on pricing tiers.

Detailed transaction approach

Seller Ledger pulls in all transaction data from Amazon via a custom-built integration. It does not require any third party connectors. And while it does pull in every Amazon transaction, it also ties every single transaction to each payout, and matches those payouts directly to your bank account deposit. This addresses the concerns about payout reconciliation, because it is built into the system, and also avoids the timing issue when a payout occurs around the end of a period.

It groups all transactions related to each Amazon order (including fees, shipping labels, etc) so you can see your net profit per order. That includes cost of goods sold, if you are using unique SKUs. Plus, it can automate inventory levels using the FIFO (first-in, first-out) method.

If you want to outsource your Amazon accounting completely, you can use Seller Ledger and invite your accounting pro to access your data. But bookkeeping services are not included in the price of the software.

Plans start as low as $10/mo for very small sellers and go up based on monthly transaction volume.

Limitations/concerns

As of the time of this writing, Seller Ledger is primarily designed for US eCommerce sellers. It handles US income and sales tax very well, but does not yet provide currency conversion. All non-US transactions are shown and summarized in their native currencies.

It is also exclusively designed for eCommerce businesses, so if you require invoicing other features for service-based businesses, you may want to look elsewhere.

Quickbooks Online or Xero + third party connector

The most familiar names in accounting software, these two classic platforms support all kinds of business types, not just Amazon businesses.

Quickbooks is by far the most popular accounting platform in the market. It has a direct integration option with Amazon, though most commentary suggests using a third party connector (A2X, Link My Books, Synder) to properly handle Amazon data. It is also more recommended for US-based businesses. However, Quickbooks is also relatively expensive and is notorious for raising prices (as in, up 35% in the last 3 years as of this writing.)

Xero has no direct integration with Amazon, relying instead on those same third party connectors. It tends to be much more recommended for non-US businesses (especially anyone based in New Zealand or Australia.) And it is quite a bit less expensive than Quickbooks.

Now let’s look at the third party connectors. While there are a lot of more general purpose middleware solutions out there (e.g. Zapier, Webgility, etc,) we are going to focus on the 3 that appear to be the best tailored for eCommerce.

A2X Accounting is well respected for their data accuracy and working especially well with Quickbooks. They use the “summarized” approach to bringing in Amazon data, though they have a creative solution for splitting payouts across periods. They are said to be a bit more complex than other solutions, and more expensive.

Link My Books, which also uses the “summarized” data approach, focuses a bit more on ease of use and VAT compliance. It is also a bit less expensive that A2X Accounting.

Synder is a more broad-based connector, working not only with Amazon and other marketplaces, but also with payment platforms like Stripe, PayPal and Square. They also support the “detailed” approach to Amazon data in your accounting platform. They tend to me a bit more complex, which, given their extra capabilities makes sense. And their pricing is a bit higher.

The combos

Given the performance and “clutter” concerns, and seeing the US vs non-US focuses, it would seem like the choices really come down to:

- Quickbooks + A2X Accounting (if you are US-based)

- Xero + Link My Books (for non-US businesses.)

In both cases, you will be using the “summarized” Amazon data approach, with the pros and cons mentioned earlier.

Both combinations are also designed very well to worth with accounting professionals.

In terms of pricing, Quickbooks Online + A2X Accounting is going to be on the more expensive side, at likely $100-$200/mo to start (depending on how many channels you link and transactions you process.)

Xero + Link My Books appears to start at about half that rate and go up from there.

One additional thought: by using two different applications, it might make for fun customer support inquiries if/when something changes or breaks. And given how often Amazon adds or changes their fees, software updates are inevitable.

Finaloop

Another relatively new option, Finaloop is a “full service” solution for eCommerce businesses looking for software + bookkeeping all in one place. Like Seller Ledger, they provide the accounting platform and a direct integration with Amazon, using the “detailed” data approach. And similar to Synder, they also link to other marketplaces and payment platforms. But their big claim to fame is that their service also comes with team members who will do your bookkeeping for you.

With pricing that starts at $250/mo, the base pricing isn’t that much more expensive than Quickbooks + A2X Accounting. But, prices rise pretty quickly and are based on your business revenue.

Limitations/concerns

Given what happened to Bench Accounting, another startup that tried to build a “software + bookkeeping” business (more broadly than eCommerce,) you’ll want to make sure you can take your data with you if needed.

Summary Comparison

Seller Ledger

Best for:

- Small to mid-sized Amazon sellers in the US

- Those who want detailed Amazon data

- Those who want an affordable option

Quickbooks + A2X Accounting

Best for:

- Scaling US-based Amazon sellers

- Those who want summary level data

- Those willing to pay for quality/reputation

- Already have an accounting pro that likes this combination

Xero + Link My Books

Best for:

- Scaling non-US based Amazon sellers

- Those who want summary data

- Those looking for a more affordable summary solution

- Already have an accounting pro that likes this combination

Finaloop

Best for:

- Amazon sellers who want to outsource their bookkeeping but don’t already have an accounting pro

- Those willing to pay for that outsourcing

- Those who want detailed Amazon data